Despite a market recently dominated by geopolitical headlines, asset classes had remained relatively stable ahead of the Federal Reserve’s latest policy meeting, supported by robust retail sales and housing data.

However, few had anticipated the assertive narrative delivered by the newly appointed Federal Reserve Chairman, Walsh.

The central bank’s “extremely hawkish turn”—reflected in both its updated dot plot and the accompanying policy statement—is poised to fundamentally reshape the valuation models for global equities, sovereign debt, foreign exchange, and commodities.

The Fed’s ‘Micro-Monetary Revolution’

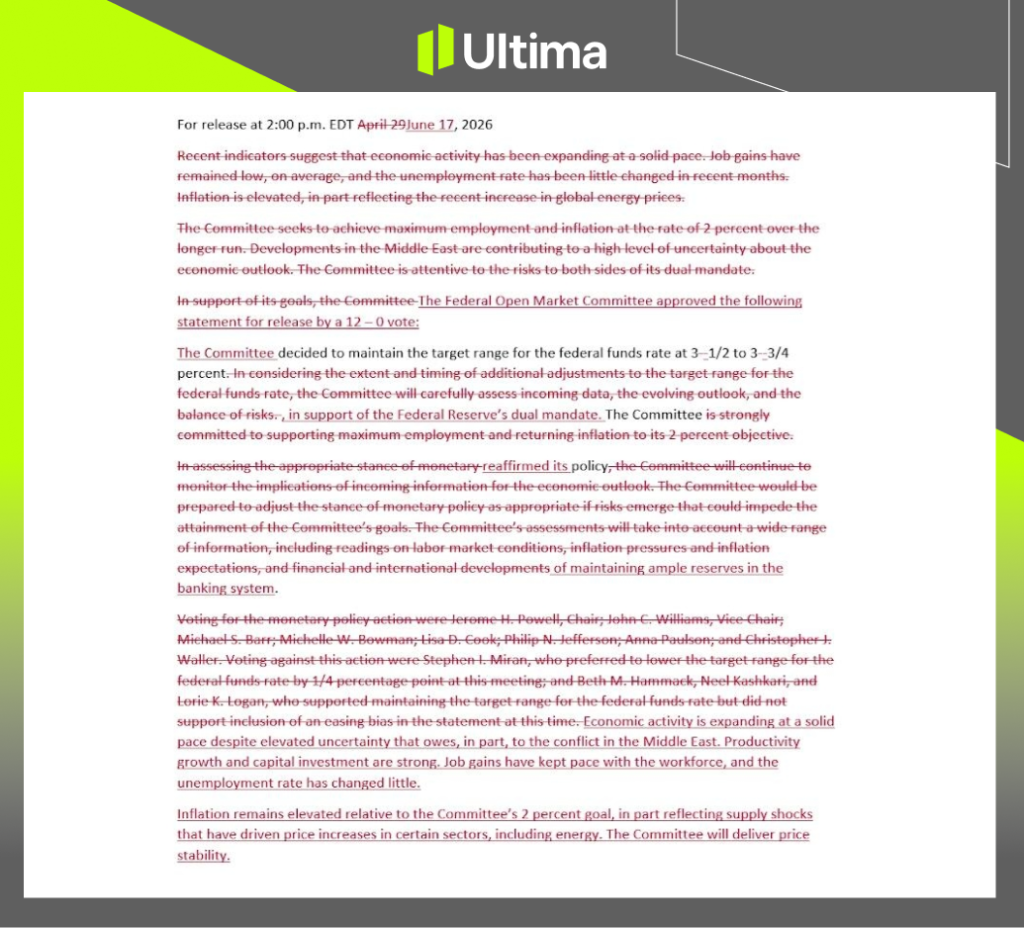

As widely anticipated, the Federal Reserve maintained its benchmark interest rate within the 3.50 to 3.75 per cent range. Yet, that was almost the sole element of the meeting that conformed to consensus.

In a statement passed by a unanimous 12-0 vote, the Federal Open Market Committee (FOMC) completely discarded its forward guidance and aggressively dismantled its remaining easing bias.

The central bank has reset its tone, adopting a simpler, more directive communication style. By abandoning much of the qualifying language of previous statements, the Fed has executed what market participants are calling a “micro-monetary revolution.”

The updated statement explicitly declared: “The Committee is committed to achieving price stability.”

Chairman Walsh clearly intends for the Fed to “explain less,” seeking to break the reflexive feedback loop between the central bank and financial markets.

Addressing the buoyant conditions across financial markets, Walsh noted directly: “Looking at what is happening in the financial markets, it is difficult for me to say that policy is currently restrictive.”

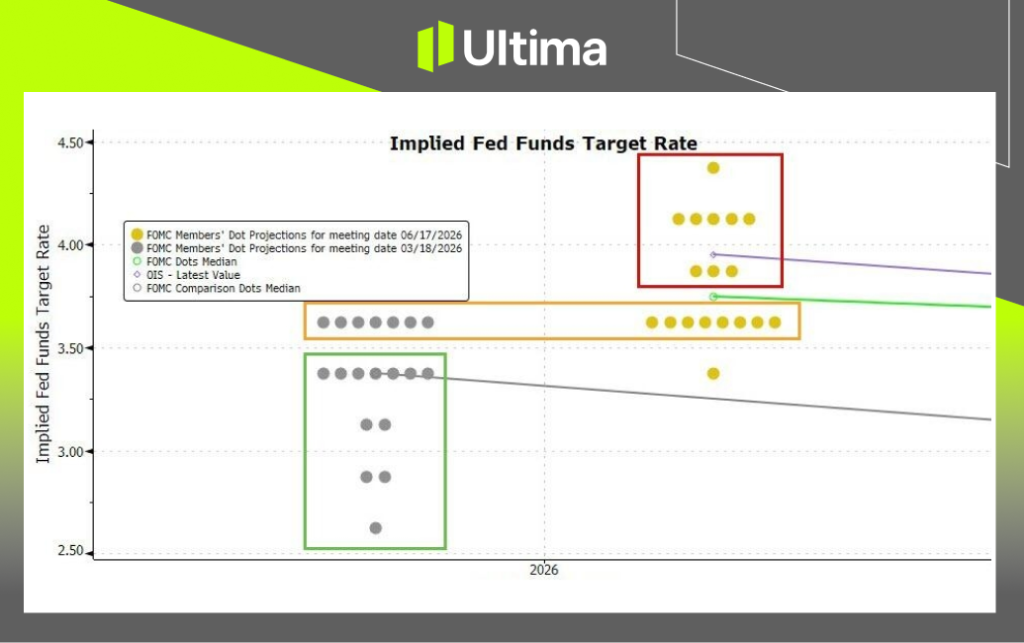

In a move that caught Wall Street off-guard, the updated dot plot revealed that nine policymakers now support at least one further interest rate hike before the end of the year.

Asset Reallocation Under a Hawkish Regime

This hawkish shift has triggered a sharp rise in market volatility. Analysts at Ultima Markets suggest that several core dimensions will dictate near-term asset performance:

1. Rate Hike Expectations Surge: The Diverging Logic of US Treasuries

The Fed’s decision has caused rate hike expectations to spike. The swap markets are now pricing in an approximate 40 per cent probability of a rate hike in July, alongside 1.5 hikes for 2026. This represents a dramatic reversal from earlier in the year, when Wall Street desks were heavily positioned for multiple rate cuts in 2026.

Consequently, short-dated Treasury yields surged, with the 2-year yield climbing 13 basis points. In contrast, long-dated bonds found solid buying support.

The underlying mechanism is straightforward: hawkish policy guidance anchors short-term rates at elevated levels, triggering a sell-off in short-dated notes as rate-cut hopes evaporate. For long-dated debt, however, a credible, hardline stance on inflation mitigates the structural risk of long-term “reflation” or unanchored price pressures.

With this primary tail risk diminished, defensive capital has flowed into long-term bonds, putting downward pressure on long-end yields.

According to charting data from the Ultima Markets MT5 platform, the price action of the 10-year US Treasury bond is currently in a consolidation phase, which could represent either a bottoming process or a continuation pattern.

(Figure: 10-year US Treasury Bond prices consolidating on MT5, Source: Ultima Markets MT5)

Market participants should focus on the key resistance level at $110 and support near $108.60. A sustained breakout in either direction is likely to establish a clear short-term trend.

2. Rising Risk-Off Sentiment in Equities: The Focus Shifts to the VIX

The Federal Reserve’s policy shift was the primary catalyst for equity market weakness on Wednesday, with all major indices closing lower and the S&P 500 underperforming.

(Figure: S&P 500 1-Hour Chart showing downward momentum, Source: Ultima Markets MT5)

Under this hawkish regime, US equity markets face a notable risk of contracting liquidity. As the summer months approach, institutional participation typically thins due to seasonal holidays. The absence of primary market makers and major desks can lead to shallower market depth.

Under these conditions, low liquidity tends to amplify market impact costs, meaning relatively small order flows can trigger outsized price fluctuations.

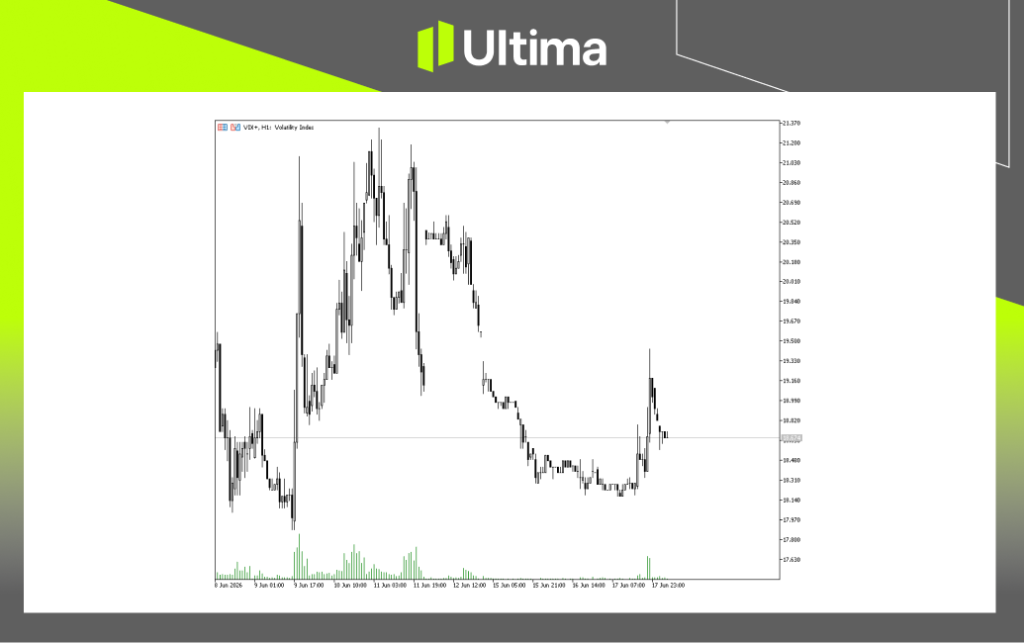

Consequently, investors should prepare for more frequent volatility and deeper shakeouts, making defensive allocations to the VIX (Volatility Index) increasingly relevant.

While the VIX has spent much of the period since April at relatively low levels, underlying factor volatility has remained elevated. The index broke back above the 18 level overnight, signaling a rapid acceleration in risk-off sentiment.

(Figure: VIX Volatility Index 1-Hour Chart breaking above key levels, Source: Ultima Markets MT5)

3. US Dollar Tests Key Resistance; Near-Term Headwinds for Gold

Supported by higher yield expectations, the US Dollar Index (DXY) rallied strongly to touch a two-month high.

From a weekly perspective, the DXY has been consolidating within a broad horizontal range for over a year. The recent move has brought the index back to the upper boundary of this range near 100.30.

(Figure: USDX Weekly Chart, Source: Ultima Markets MT5)

Should the index secure a clean breakout above this resistance, it is highly likely to extend its gains toward the 200-week moving average near 101.80.

The combination of a stronger dollar and higher rate expectations pushed Gold prices back below the $4,250 per ounce threshold, effectively erasing the gains accumulated earlier in the week on geopolitical easing hopes.

Despite a modest intraday bounce during Thursday’s Asia-Pacific session, a structural near-term reversal remains unlikely, given the stronger dollar and overhead technical resistance from the 200-day moving average.

(Figure: Gold Daily Chart testing lower boundaries, Source: Ultima Markets MT5)

Summary

The “micro-monetary revolution” of the Walsh era has officially commenced. The deliberate removal of forward guidance means that market volatility is likely to be fully unleashed.

In this new phase of resurgent rate expectations and tightening liquidity, reassessing asset allocations, monitoring the VIX, and identifying critical technical support and resistance levels will remain paramount for capital preservation.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.