This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

May NFP Consensus ‘Deeply Fractured’ Ahead of Potential Market Turmoil

May NFP Consensus ‘Deeply Fractured’ Ahead of Potential Market Turmoil

The attention of global financial markets is firmly fixed on the release of the US non-farm payrolls (NFP) report for May, due to be published today.

For market participants, this release represents far more than a routine economic data point; it is expected to dictate the Federal Reserve’s next policy moves and trigger substantial volatility across foreign exchange and sovereign debt markets.

Yet, at this critical juncture, Wall Street remains unusually and deeply divided.

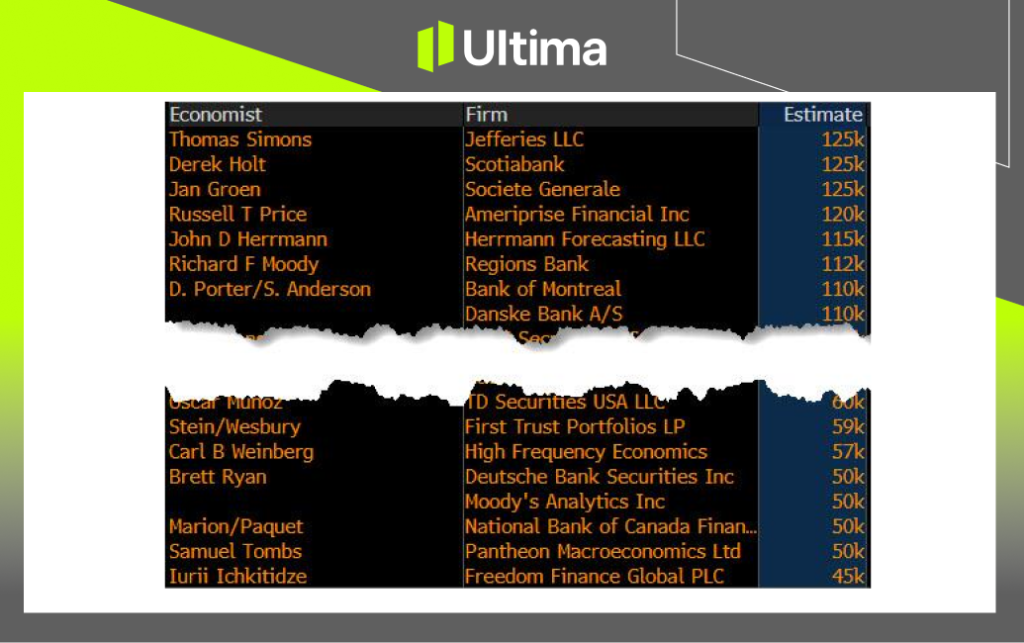

A Fractured Consensus: 60,000 or 95,000?

There is currently no unified script across institutional desks regarding the headline May payrolls figure.

While the broader market consensus points to an increase of between 85,000 and 88,000 jobs—representing a notable deceleration from the previous month—the range of individual forecasts is exceptionally wide, spanning from a pessimistic 45,000 to a highly optimistic 125,000.

The bearish camp expects the headline print to land near 60,000, with private-sector payrolls adding a modest 65,000. Proponents of this view point to cooling alternative employment indicators, a persistent government hiring freeze, and localized strike action (estimated to have dragged figures down by roughly 2,600) as key headwinds.

Conversely, the bullish camp is confident that job growth will reach 95,000 or more. Their optimism is underpinned by stable initial jobless claims, early summer hiring linked to sporting events, and resilient recruitment in service sectors such as education, healthcare, and leisure and hospitality.

This stark divergence in forecasts has elevated market tension ahead of the release.

Underlying Reality: The ‘Low-Hiring, Low-Firing’ Deadlock

The reason behind this extreme market division lies in the highly contradictory signals emerging from underlying labor market data.

On one hand, corporate layoffs remain remarkably low. Average initial jobless claims during the survey month fell below the prior month’s average, while overall layoff rates continued to trend lower. This forms the foundation of the argument for labor market resilience.

On the other hand, corporate appetite for fresh hiring is cooling rapidly. Business surveys, including the employment sub-indices of both the ISM Services and Manufacturing purchasing managers’ indices (PMIs), have consistently registered in contractionary territory.

The Federal Reserve’s latest Beige Book highlighted this reality, describing a “low-hiring, low-firing” environment where firms are becoming highly selective, implementing hiring freezes, or opting not to replace departing staff.

The Real Anchors: Unemployment and Wages

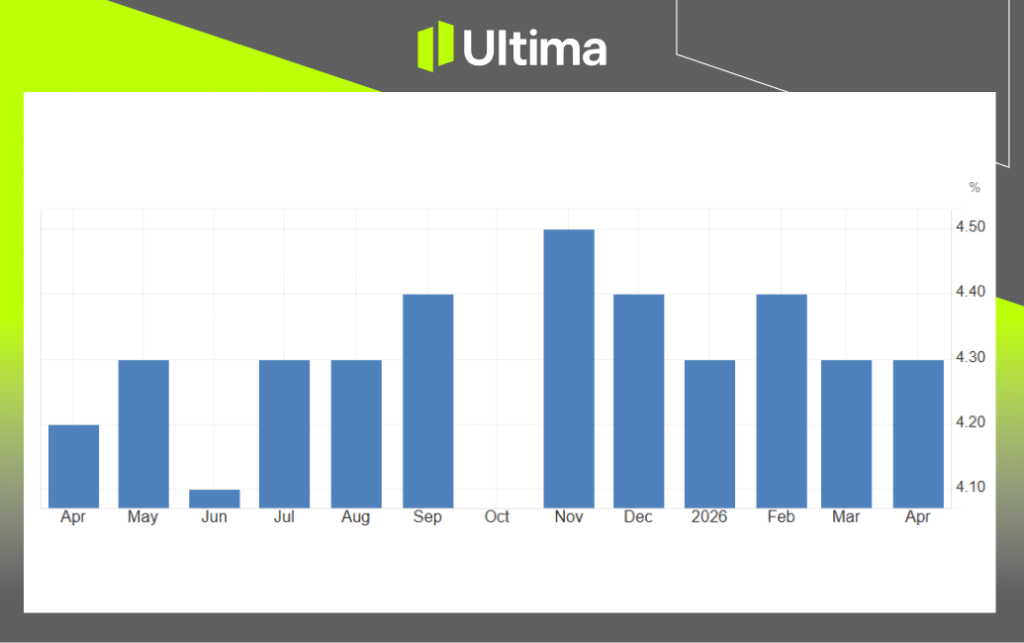

Rather than the headline payroll number, the unemployment rate—currently projected to round to 4.3 per cent—may serve as the primary anchor for market pricing.

Analysts suggest that as long as the unemployment rate remains at 4.3 per cent or below, the Federal Reserve will feel comfortable maintaining its current policy stance. A move back towards 4.0 per cent would likely be required before further interest rate hikes could be realistically priced back in.

However, the risk remains tilted to the upside. The unrounded unemployment rate stood at 4.34 per cent last month—just shy of the 4.4 per cent threshold—and May typically introduces modest seasonal upward pressure on the data.

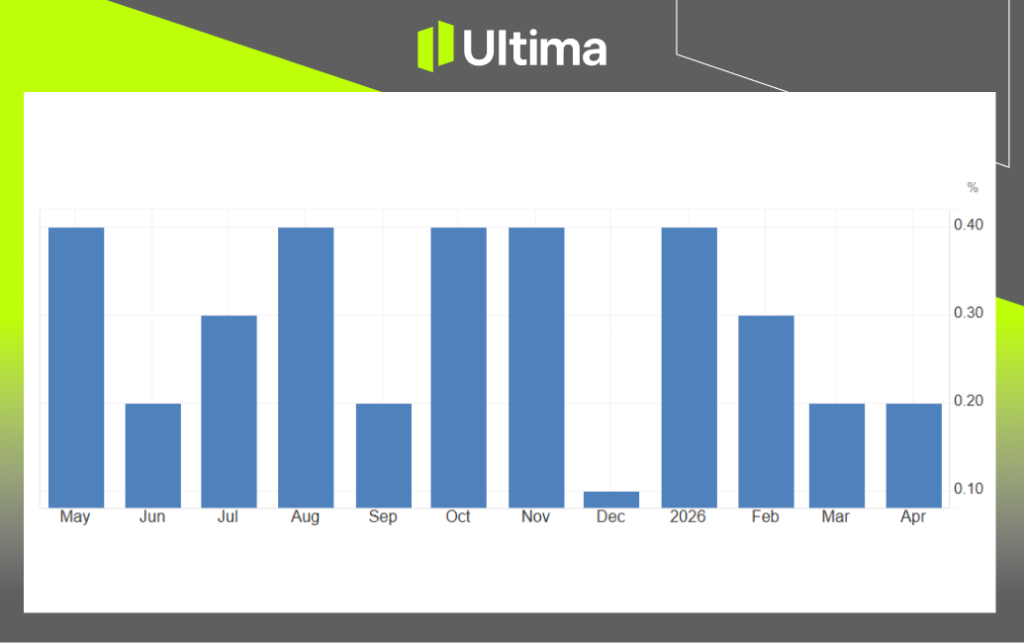

Average hourly earnings also present a potential inflation risk. Supported by calendar effects, average hourly earnings are forecast to rise by 0.3 to 0.4 per cent month-on-month, while wage growth for job-switchers in the private sector remains elevated.

The ghost of inflation has clearly not yet departed the labor market.

Market Positioning: Bonds, Currencies, and Equities

The impact of this payroll report on global asset classes is expected to be highly asymmetric, with stronger-than-expected data likely to cause far greater disruption than a soft print.

Government Bonds

Should the payroll data exceed forecasts, US Treasury yields are likely to surge more aggressively than they would retreat in the event of a weak print.

(Figure: 10-year US Treasury prices consolidating within a symmetrical triangle, Source: Ultima Markets MT5)

Options pricing suggests that the implied daily move for the 10-year US Treasury yield is roughly 5.5 to 6 basis points—significantly higher than historical averages.

Given that the market has recently adjusted its expectations toward higher interest rates over the coming year, a robust print could further increase the perceived probability of policy tightening.

Foreign Exchange

The US dollar has recently been driven primarily by geopolitical developments and oil price volatility, leaving the index confined to a narrow range.

(Figure: US Dollar Index trading in a sideways consolidation pattern since 20 May, Source: Ultima Markets MT5)

However, a strong employment print has the potential to break this quiet period, reigniting the dollar’s upward momentum and reinforcing upside risks.

Equities

US stock markets find themselves facing a difficult dilemma.

Scenario analyses indicate that equity investors would heavily favour a “Goldilocks” print (roughly 70,000 to 100,000 new jobs), which would likely support a modest rally.

However, a very weak print (below 40,000) could spark stagflation anxieties, while an overly strong print (above 130,000) would drive bond yields higher, putting significant pressure on equity valuations.

(Figure: Nasdaq 100 index exhibiting a potential topping pattern, where higher bond yields could further weigh on technology stocks, Source: Ultima Markets)

In summary, the market is no longer simply trading a single headline figure. The key issue is whether the combination of job growth, the unemployment rate, and wage inflation collectively points to a tight labor market.

If the data confirms this tightness, bond yields and the US dollar are poised to lead the reaction, leaving equity investors to navigate the delicate balance between resilient economic growth and the threat of prolonged policy tightening.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.