This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Fed’s Case for July Hold: Cooling Jobs, Falling Oil & Sticky Prices

Fed’s Case for July Hold: Cooling Jobs, Falling Oil & Sticky Prices

Three numbers landed within weeks of each other in mid-2026, and read together they tell a more coherent story than any one of them tells alone. A stubbornly soft June jobs report, a wholesale price index still running hot from May, and a sharp reversal in oil prices appear, on the surface, to pull in different directions. Read as a sequence, though, they point to the same conclusion for the Federal Reserve’s July meeting: hold steady.

A Labor Market Losing Steam

Start with the headline news. Nonfarm payrolls, released July 2, rose by just 57,000 in June — well short of the 110,000 to 114,000 economists expected, and one of the weakest monthly prints in recent years. The result lines up closely with the trailing 12-month average of roughly 36,000 jobs per month, and it came alongside downward revisions to April and May totaling a combined 74,000 jobs, underscoring that hiring momentum has been fading for longer than the June number alone suggests.

The composition matters as much as the headline. Professional and business services added 36,000 jobs, social assistance added 25,000, and health care added 22,000 — sectors that have carried job growth for months. Leisure and hospitality, by contrast, shed 61,000 positions amid weaker seasonal hiring. The unemployment rate held at 4.2%, with little movement in labor force participation, and average hourly earnings rose a moderate 0.3% to $37.64, up 3.5% year-over-year — a pace that shows no sign of a wage-price spiral.

Taken together, this is a labor market that is cooling but not cracking: no broad-based layoffs, but clearly less heat than earlier in 2026. For the Fed, that matters most as a signal about demand. A slower-hiring economy is one less likely to overheat, which lowers the odds that policymakers would need to raise rates to cool things further.

Producer Prices Sound the First Alarm

While the labor market was cooling, price data from earlier in the spring told a hotter story — and it starts upstream, at the producer level. The Producer Price Index (PPI) for final demand rose 1.1% month-over-month in May and 6.5% year-over-year, the strongest annual pace since late 2022. Energy goods jumped 10.7%, and gains were broad-based across both processed and unprocessed goods, signaling that cost pressure was building across the supply chain. Core PPI, which strips out food, energy, and trade services, advanced 0.8% — its strongest reading in years.

PPI is worth watching precisely because it tends to lead. Costs incurred by producers and wholesalers typically show up in consumer prices with a lag of one to three months, as businesses pass expenses through gradually rather than all at once, and as margins and substitution effects blunt some of the impact along the way.

The Pass-Through Confirms Itself at the Register

That lag is exactly what shows up next in the Personal Consumption Expenditures (PCE) price index — the Fed’s preferred inflation gauge, and the consumer-facing counterpart to PPI. PCE rose 0.4% in May, putting the headline rate at 4.1% year-over-year. Core PCE, which excludes food and energy, rose 0.3% for the month and 3.4% annually — the highest core reading since late 2023.

The connection to the producer-side data is direct: May’s PPI surge, driven largely by energy, lines up with firmer energy components in PCE and an overall reacceleration in consumer prices. Together, the two reports describe a single pipeline — cost pressure entering at the wholesale level and reaching households a month or two later — rather than two unrelated stories.

Then Oil Changed the Script

Here is where the picture shifts. Both the PPI and PCE readings above are May data, capturing a period when oil prices were still elevated following Strait of Hormuz disruptions that had pushed Brent crude to a peak near $118 to $120 a barrel. Since then, oil has fallen sharply. Brent has retreated to around $72 a barrel — back to pre-conflict, late-February 2026 levels — while WTI hovers near $69 to $71. Gasoline futures have eased in step.

Because the PPI and PCE reports available now predate this decline, the energy-driven portion of May’s price pressure has not yet had the chance to unwind in the official data. Given the one-to-three-month pass-through window described above, that relief should begin showing up in the PPI and PCE prints covering June and July.

Three Data Points, One Signal

Put the three releases in sequence and a single narrative emerges. Producer prices in May showed cost pressure building, concentrated in energy. PCE confirmed that pressure was passing through to consumers on the usual lag, pushing core inflation to its highest level since late 2023. But the energy shock behind much of that pressure has since reversed, which — if the same one-to-three-month transmission lag holds on the way down as it did on the way up — should start easing headline and possibly core readings in the coming months.

Meanwhile, the labor market is doing its own part to keep inflation risk contained from the demand side. A payrolls report this soft, with wage growth holding near 3.5% rather than accelerating, reduces the chance that a tight labor market pushes prices higher independently of what energy is doing. The risk that remains is that core PPI and core PCE — the measures that exclude energy — are still elevated on their own merits, which means the disinflation story is not yet complete even as the energy piece improves.

What This Means for the Fed

For the Federal Reserve, these three threads argue for patience rather than action. The soft jobs data removes the case for a hike: there is little evidence of an overheating economy that needs cooling. At the same time, May’s core PPI and core PCE readings — still running hot — argue against a cut, since the underlying inflation picture has not yet shown a clear, sustained downturn independent of energy swings. Cutting now, before it is clear whether falling oil prices translate into softer core readings or whether pass-through proves stickier than the historical lag suggests, risks reigniting inflation expectations prematurely.

The most likely path, then, is a hold at the July meeting. That gives policymakers room to watch two things play out over the next several data cycles: whether core inflation moderates as the oil-price relief works its way through the PPI-to-PCE pipeline, and whether labor market slack continues to build. A hold preserves the Fed’s optionality while the economy works through this soft patch — cooling on the jobs side, still digesting a price shock on the inflation side, and waiting for the two to reconcile.

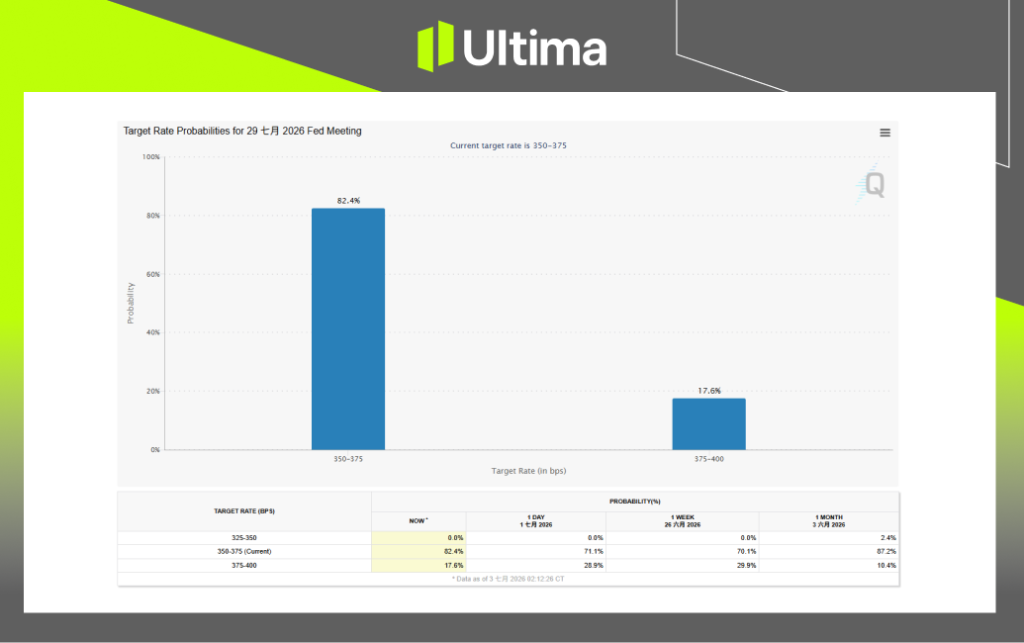

On the Fedwatch interest rate forecasting tool, the probability of a rate hike stood at 29.9% a week ago, but plunged to 17.6% after the nonfarm payrolls release.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.