This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Copper’s Structural Shift: From Cyclical Metal to Strategic Asset

Copper’s Structural Shift: From Cyclical Metal to Strategic Asset

As of early 2026, copper has effectively decoupled from traditional construction and economic cycles. The market narrative has shifted decisively, from what was once framed as a temporary supply shortage to a structural deficit that could define the copper market for the next decade.

With prices shattering records in January 2026, COMEX copper futures briefly surging above $6.49/lb—the red metal has transitioned from a cyclical industrial indicator into a strategic asset at the heart of global electrification and technological transformation.

This raises two critical questions for investors and traders:

What is truly driving copper prices higher?

Is this price level sustainable through 2026?

To answer these, we need to examine copper’s demand transformation, supply constraints, and the growing sources of volatility ahead.

Demand Drivers: The New “Big Three”

Copper’s 2025–2026 rally is not driven by a single theme, but by a structural paradigm shift powered by three long-duration demand engines. Together, they have reshaped copper’s demand profile into one that is far less sensitive to traditional economic slowdowns.

1. AI & Data Centers: The Second Electrification

The global rollout of artificial intelligence infrastructure has triggered what many analysts now call a “second electrification wave.”

AI-focused data centers require 3-5 times more copper than conventional facilities due to high-density power distribution, advanced cooling systems and redundant electrical wiring for reliability

Major technology firms such as Microsoft, Google, and Amazon have effectively become large-scale copper consumers, creating a new demand floor that is significantly less sensitive to interest rate cycles.

Industry estimates suggest that AI and data center expansion alone could account for approximately 475,000 tonnes of copper demand by 2026, a figure that did not meaningfully exist just a few years ago.

2. Grid Modernization & Energy Transition

Beyond AI, copper demand is being structurally reinforced by global grid modernization.

Over 60% of incremental copper demand growth through 2030 is projected to come from power infrastructure upgrades. The rapid integration of renewable energy sources, incuding solar, wind, and energy storage requires:

Higher-capacity transmission lines

More resilient distribution networks

Expanded interconnection infrastructure

Unlike traditional construction demand, this segment is policy-driven and non-discretionary, making it far more resistant to cyclical slowdowns.

3. Transportation Electrification

Electric vehicles remain a core pillar of copper demand. While overall auto sales growth has moderated, copper intensity per vehicle continues to rise.

An electric vehicle requires approximately four times more copper than an internal combustion engine (ICE) vehicle (roughly 80–100kg per unit) due to batteries, motors, inverters, and charging infrastructure.

Even in a cooling auto market, this structural shift ensures that copper demand from transportation remains robust.

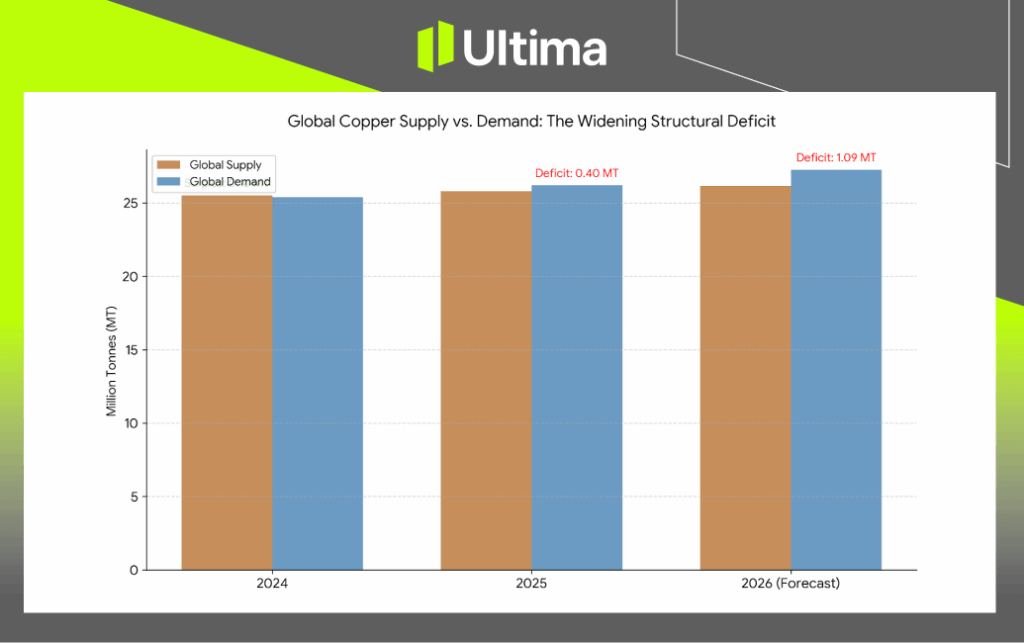

Supply Constraints: A System Struggling to Keep Up

While demand accelerates, supply is failing to respond. This is not merely a case of tight inventories; the copper market is facing a structural supply problem driven by operational setbacks, geological challenges, and underinvestment.

Key Supply Headwinds

Grasberg Mine (Indonesia): The world’s second-largest copper mine continues to recover from the September 2025 mudslide, which triggered a force majeure event. Remediation remains ongoing, with only a phased restart expected in the second half of 2026. Full capacity is unlikely before 2027, leaving a significant gap in global refined supply.

Chile’s Aging Assets: Major producers such as Codelco and Antofagasta are battling declining ore grades. In some cases, miners now need to process 40–60% more material to extract the same amount of copper, sharply increasing All-In Sustaining Costs (AISC) and limiting output growth.

Global mine supply growth for 2026 is struggling to reach 1.4%, while annual demand growth is accelerating toward 3–4%. This widening gap underpins the structural bull case for copper.

Copper Supply Deficit | Chart Source: Ultima Markets

Risks & Volatility: When Prices Get “Too Right”

While the fundamental imbalance strongly supports higher prices, no commodity bull market is linear. Elevated prices introduce their own risks, particularly when they push demand behavior beyond rational thresholds.

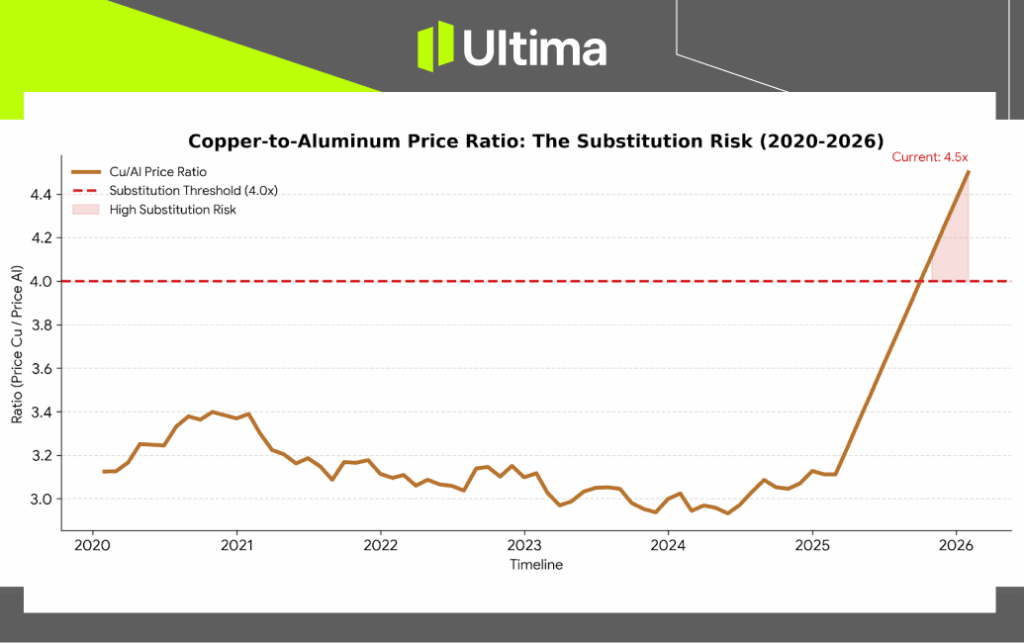

1. The Substitution Risk: Copper vs. Aluminum

Historically, when the copper-to-aluminum price ratio exceeds 4.0:1, manufacturers begin actively substituting aluminum in wiring and components where technically feasible.

As of early 2026, the ratio has stretched to approximately 4.5:1, placing copper firmly in the danger zone.

Copper: Aluminium Ratio Trend | Data Source: COMEX/LME | Chart: Ultima Markets

If COMEX copper prices sustain levels above $5.90/lb, long-term demand destruction via aluminum substitution—especially in power transmission and automotive applications—could begin to offset gains from electrification and AI infrastructure.

In this sense, “Dr. Copper” risks becoming too expensive for its own diagnosis.

2. The June 30 Tariff Cliff

Another major source of near-term volatility lies in U.S. trade policy.

The U.S. Department of Commerce faces a June 30, 2026 deadline to decide whether to recommend 15–25% tariffs on refined copper imports.

In anticipation, traders and consumers may front-load copper shipments into U.S. warehouses to avoid potential tariffs—temporarily inflating demand and prices.

The risk: If tariffs are delayed or ultimately rejected, this inventory overhang could unwind rapidly, triggering a sharp—but likely temporary—price correction toward the $5.00/lb region.

3. Precious Metals Spillover: The “Red Gold” Effect

Finally, copper may also be benefiting from cross-asset momentum.

With gold and silver experiencing parabolic rallies and record highs, investors have increasingly grouped copper into the broader hard-asset and de-dollarization narrative.

While copper is not a precious metal, its role in electrification, energy security, and strategic infrastructure has earned it the nickname “red gold.” Part of the 2026 surge may represent a secondary wave of capital rotation flowing out of precious metals into industrial metals with strategic value.

Outlook: Structural Bull, Tactical Volatility

Copper’s transformation from a cyclical industrial metal into a strategic commodity is both real and durable. The expansion of AI infrastructure, the global energy transition, and transportation electrification have fundamentally reshaped copper’s demand profile, while supply constraints remain deeply entrenched and slow to resolve.

That said, elevated prices introduce non-linear risks, particularly from material substitution and policy-driven inventory distortions.

Based on the historical 4:1 copper-to-aluminum ratio, copper’s fair value sits around USD 4.3–4.5 per lb, beyond which substitution risk rises. Adding a structural premium from AI and electrification demand brings a reasonable equilibrium range to USD 5.0–5.3 per lb. Prices above this range may see tactically volatile pullbacks through 2026, particularly amid policy uncertainty and price-sensitive demand adjustments.

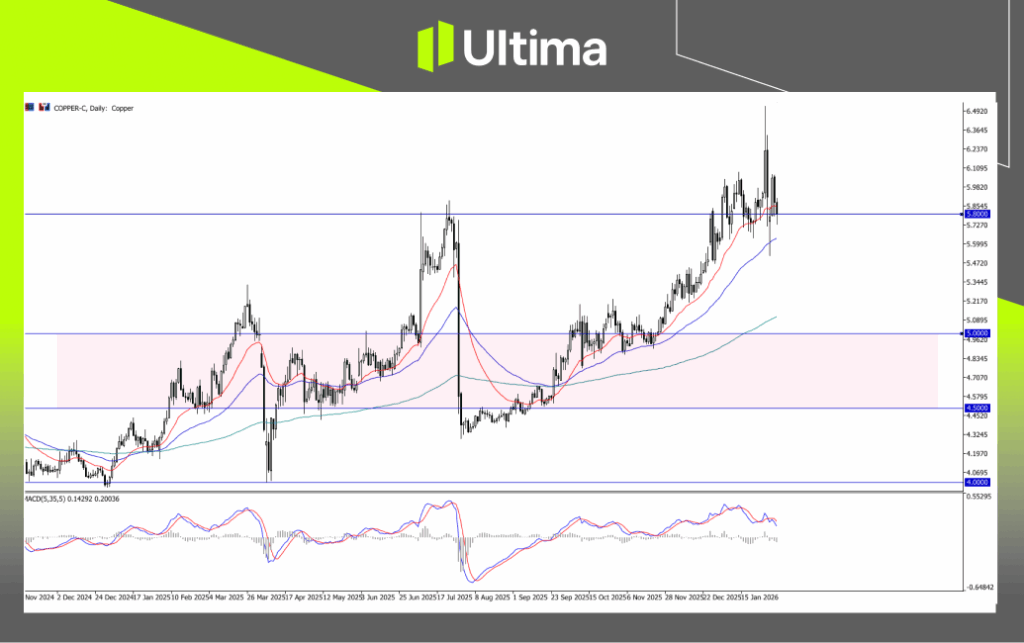

Copper-C, Daily Chart | Source: Ultima Markets MT5

Recent price action signals the potential for a recalibration following the parabolic surge to $6.49/lb.

Support: $5.80/lb remains a key level; a break below could trigger a corrective move.

Resistance / Critical Barrier: $6.0/lb on is a psychological level where substitution risks and inventory flushes could meaningfully impact the bull run.

The bottom line?

While the structural deficit remains the long-term story, 2026 will be defined by policy volatility and price sensitivity. For investors and traders, copper is no longer just an economic indicator—it is a macro asset, demanding both conviction and risk discipline.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.