This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

The Warsh Era Begins: the Next Cross-Asset Supercycle

The Warsh Era Begins: the Next Cross-Asset Supercycle

With the US Senate officially confirming his nomination, the Federal Reserve has formally closed the book on the Jerome Powell-led years, ushering in the “Warsh Era.”

A pervasive misconception among retail investors is that a new Fed Chair—especially one nominated by Donald Trump—automatically equates to aggressive rate cuts, relentless liquidity injections, and an equity market melt-up.

The financial reality is far more complex. The Fed Chair serves as a profound amplifier of market sentiment, but the ultimate driver of asset prices remains the macroeconomic inheritance they step into.

As Kevin Warsh takes the helm in a deeply complex economic environment, how will his doctrine reshape monetary policy, and what are the underlying structural shifts occurring across global asset classes?

I. Decoding Warsh: The Death of Forward Guidance

To forecast future asset trajectories, the market must first categorize Warsh. Is he a hawk or a dove? The answer defies simple binary labels.

As a former Fed Governor and seasoned economic advisor, Warsh brings a distinctly pragmatic, action-oriented approach to the central bank.

Anti-Forward Guidance: Warsh is deeply critical of the excessive “forward guidance” that defined the Powell era, arguing that constant verbal intervention exacerbates market volatility.

Back to Basics: He advocates for a strict adherence to the Fed’s dual mandate—price stability and maximum employment—while explicitly rejecting mission creep into areas like climate change or green energy policy.

Anti-QE: Most crucially, Warsh is a staunch opponent of Quantitative Easing (QE) and open-ended balance sheet expansion. He favors structural institutional adjustments over massive bond-buying programs to manage interest rates.

The Powell Shadow: Complicating the narrative is a dramatic institutional twist. While stepping down as Chair, Powell has opted to remain on the Board of Governors. This preserves a formidable hawkish voting bloc within the FOMC.

Any political ambitions to force immediate rate cuts will face an ironclad wall of resistance from within the committee.

II. The Macro Repricing: Zero Rate Cuts and the “Higher for Longer” Reality

Warsh inherits an incredibly thorny macroeconomic landscape:

Sticky Inflation: Recent headline and core CPI prints have both surprised to the upside. Geopolitical supply chain disruptions have directly inflated energy costs, creating secondary inflationary waves across agricultural commodities and freight.

Labor Market Bifurcation: While aggregate unemployment appears stable, the underlying structure is shifting. The rapid deployment of AI is accelerating labor displacement, leading to quiet contractions and layoffs in traditional sectors.

Caught between entrenched inflation and a bifurcated labor market—and facing a hawkish FOMC holdover—the market is currently undergoing a violent repricing. Expectations for rate cuts this year have effectively evaporated. More aggressively, Fed Funds futures are now beginning to price in the tail risk of one to two rate hikes next year.

III. The Warsh Era Playbook: Where Should Investors Allocate?

Under the regime of “Higher for Longer” (and potentially higher yet), cross-asset performance will diverge sharply. Here is the strategic roadmap:

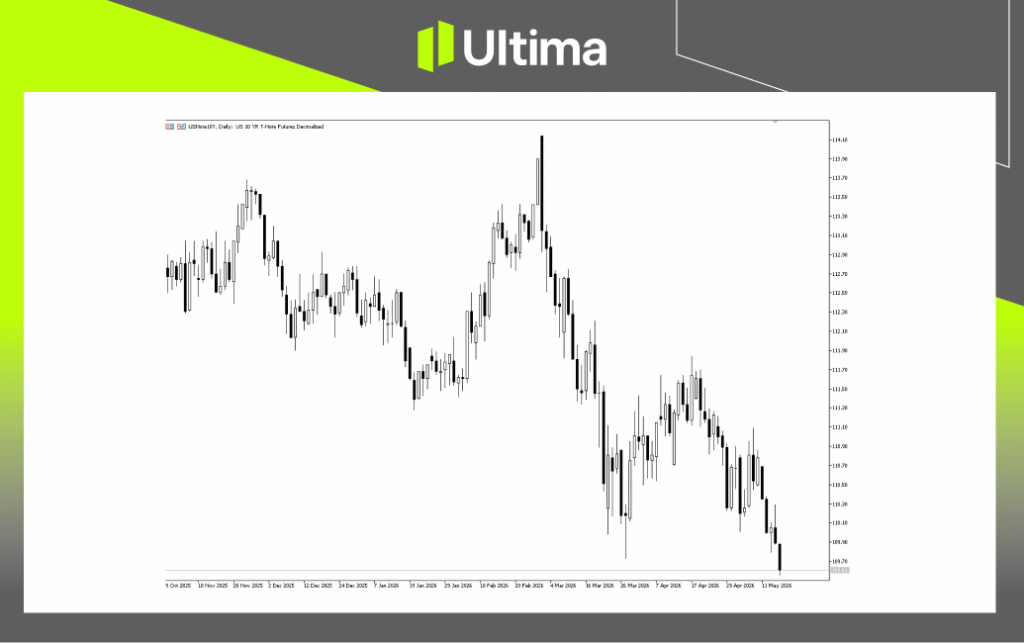

1. The North Star: The 10-Year US Treasury

Warsh is a central banker who deeply respects the bond market’s signal. For the next 12 to 24 months, regardless of whether you are trading equities, gold, or crypto, the 10-year Treasury yield is your daily dashboard.

In an environment where the Fed is biased toward holding or hiking, liquidity will seek yield, leading to structural selling pressure on bonds.

Consequently, the fundamental path of least resistance for Treasury prices is down (yields up). From a risk-reward perspective, any tactical rally in Treasury prices (hitting technical resistance) presents a high-probability opportunity to fade the move (sell the rips).

Persistently high Treasury yields will continue to act as a gravity well, suppressing the valuation multiples of long-duration assets.

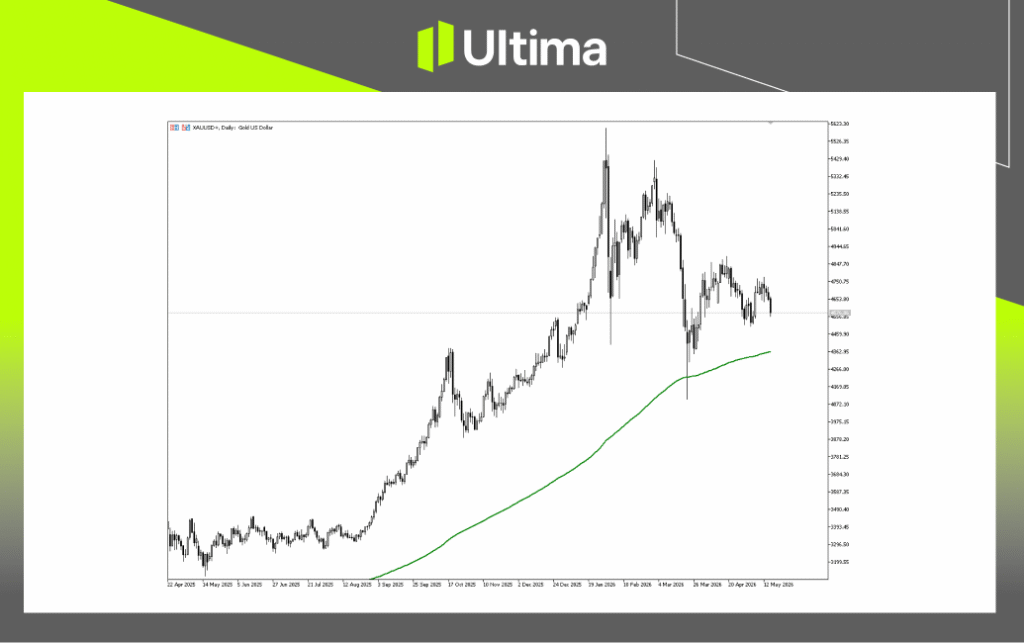

2. The Ultimate Hedge: The Long USD / Long Gold Barbell

Orthodox textbook economics suggests that high rates bolster the Dollar and crush Gold. Yet, the current Dollar index action is heavily conflicted.

Why? Because the market is pricing in not just interest rates, but the credibility of the US fiscal trajectory.

As global confidence in US fiscal sustainability wavers and foreign exchange reserves diversify, capital is structurally migrating into Gold. Global central banks remain relentless dip-buyers. As long as US deficit spending remains unabated, the secular bull case for Gold is unbreakable.

However, intermittent Treasury price rebounds will temporarily cap Gold’s momentum, resulting in choppy, consolidating price action.

Utilize the 200-day moving average (DMA) as a structural compass. Accumulate Gold on dips below the 200-DMA, and trim positions tactically as it deviates toward previous highs.

Concurrently holding both Long USD and Long Gold positions creates a sophisticated, asymmetric macro hedge.

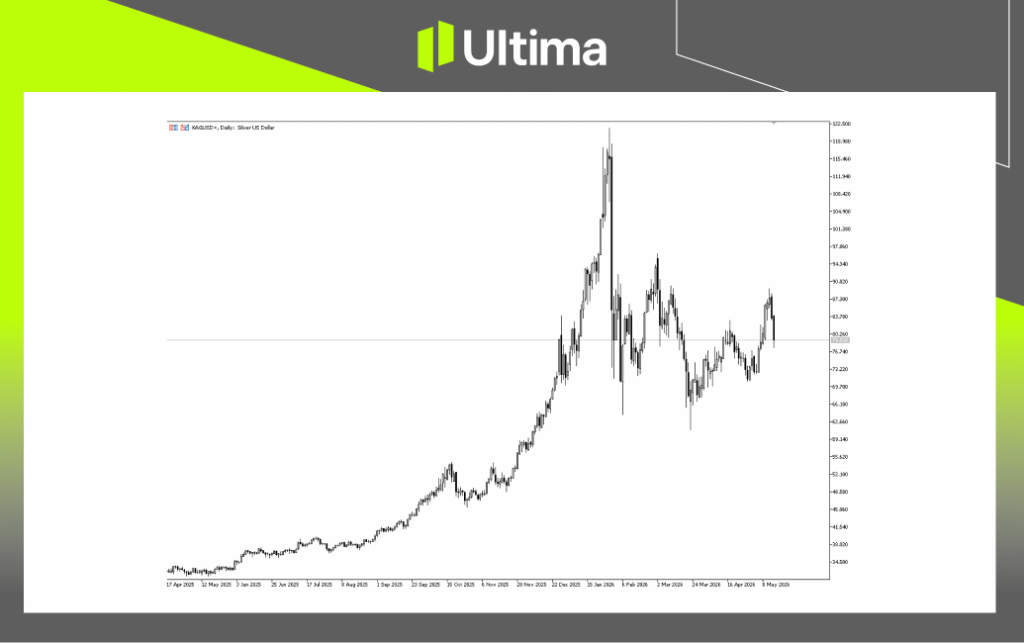

3. The AI Decoupling: Equities and Industrial Metals

Historically, crude oil spikes and geopolitical kinetic wars would derail US equities. Not anymore.

The broader US market has decoupled, driven entirely by the AI semiconductor supercycle and robust mega-cap tech earnings. The market has prematurely priced in eventual geopolitical ceasefires, rendering it remarkably immune to short-term macro headwinds.

This AI narrative is directly fueling a parallel boom in industrial metals (Copper, Silver, Aluminum), which are printing fresh highs. The fundamental catalyst is the unprecedented physical demand for conductive metals required to build out global AI data centers and server farms.

Copper and Silver are highly sensitive to institutional warehouse inventories and spot market squeezes, making them prone to violent volatility.

Investors should approach these markets with tactical swing trading strategies rather than rigid “buy-and-hold” assumptions.

Conclusion

The “Warsh Era” will not be a continuation of the free-liquidity party; it is a long-term chess game that will test investor discipline.

Discard any lingering fantasies of spontaneous rate cuts and respect the resilience of inflation. By anchoring your portfolio to the Treasury market’s signals, hedging macro tail risks with Gold, and tactically trading the AI-driven industrial boom, investors can navigate this new central banking regime with confidence.

Disclaimer

The comments, news, research, analysis, prices, and other information contained herein are provided as general market information only, to assist readers in understanding market conditions, and do not constitute investment advice. Ultima Markets has taken reasonable measures to ensure the accuracy of this material, but cannot guarantee its precision, and it may be changed at any time without notice. Ultima Markets will not accept liability for any loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.