This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Central Bank Hawkish Pivot: What It Means for Global Markets

Central Bank Hawkish Pivot: What It Means for Global Markets

The global monetary landscape underwent a seismic shift during the March 2026 “Super Central Bank Week.” What began the year as a coordinated “glide path” toward rate cuts has abruptly pivoted into a defensive “Hawkish Hold.”

This transition is driven by a dual-threat environment: stubbornly high domestic services inflation and a massive geopolitical risk premium in the energy markets following the escalation in the Middle East.

This shift is set to significantly redefine the global market landscape for the coming months.

Central Banks: A Unified Front of Caution

The major central banks meeting this week converged on a single narrative: a “Hawkish Hold” fueled by caution on the inflation front as energy market shocks from Middle East tensions ripple through the supply chain.

Federal Reserve: The “Higher for Longer” Anchor

The FOMC maintained the federal funds rate at 3.50%–3.75% as widely expected. However, the accompanying message and forecasts were decidedly hawkish, representing a total reversal from just months ago when cuts were the base case.

The Hawkish Shift: While the median “dot plot” still technically suggests one cut in 2026, Chair Powell admitted there was significant movement toward no cuts at all this year.

Economic Revisions: The Fed raised its 2026 GDP growth forecast to 2.4% (up from 2.3%) and pushed its core PCE inflation projection up to 2.7%.

Powell explicitly noted that the Fed cannot ignore “energy-induced inflation” if it threatens to unanchored long-term expectations. This signals that the “Fed Put” is currently off the table, as dot plot projections were significantly adjusted upward.

Developments Across Other Major Central Banks:

Bank of Japan (BoJ): The BoJ held rates at 0.75%, but the meeting was defined by a rare 8-1 split vote. Hawkish board member Hajime Takata dissented, calling for an immediate hike to 1.0% to combat escalating upside price risks and currency weakness.

Bank of England (BoE): In a unanimous vote, the BoE kept the Bank Rate at 3.75%. The Committee officially “shelved” its previously planned spring rate cut and warned that the energy shock could push UK CPI back toward 3.5% in Q3—a dramatic reversal from the 2% target path seen last month.

Reserve Bank of Australia (RBA): The RBA stood out as the most aggressive, delivering a 25bps hike to 4.10%. Governor Bullock cited “material risks” that inflation would remain above the 2–3% target band until 2027, necessitating immediate action.

Notably, only the Swiss National Bank (SNB) remained on the dovish side, citing concerns over currency strength and its deflationary impact on the Swiss economy.

The April Market Landscape: What’s Next?

As we move into April, the market narrative is expected to transition from pure “Fed-watching” to a broader focus on “Oil-watching” and Global Yield dynamics. Three critical themes are likely to dominate the financial landscape:

Energy Volatility: If Brent crude remains sustained above $110/barrel, expect further hawkish repricing across the board. This environment will remain particularly challenging for risk assets, with the equities market facing a “valuation squeeze” as input costs rise and the discount rate remains elevated.

Inflation Risk: Persistent energy volatility translates directly into renewed inflation risk. This complicates the global central bank pivot; as most central banks maintain a “hawkish hold,” the prolonged period of high interest rates creates a restrictive environment that is inherently negative for growth-sensitive sectors.

Global Yields: We are witnessing a significant shift in the yield curve. Short-term yields are surging as markets aggressively price out 2026 rate cuts, while long-term yields rise on fears of “sticky” inflation. This upward pressure puts immense strain on government debt valuations, weighs on risk assets, and triggers heightened volatility in global currency pairs (particularly the Yen and Euro).

Impact on Global Yields, Gold, and Equities

The shift in monetary policy has triggered an immediate and aggressive repricing across global asset classes. This was most visible in the “blood bath” following the central bank announcements, as markets realized the “pivot” they had been hoping for was effectively dead.

1. Gold Face Pressure on Yield

Gold, which had been hovering near the psychologically critical $5,000/oz mark for much of the past month, faced heavy selling pressure following the “Super Week.” This is no coincidence; as a non-yielding asset, Gold is highly sensitive to the real yield environment.

Yield vs. Zero-Coupon: The sharp rise in sovereign yields has increased the opportunity cost of holding Gold. With the USD strengthening alongside yields, Gold is being hit by a “double whammy.”

The Bear Cycle Risk: Having reached record-high levels earlier this year (peaking near $5,400), Gold is now entering a vulnerable correction phase. If yields remain “higher for longer,” Gold could undergo a sustained bear period as institutional investors rotate back into fixed income.

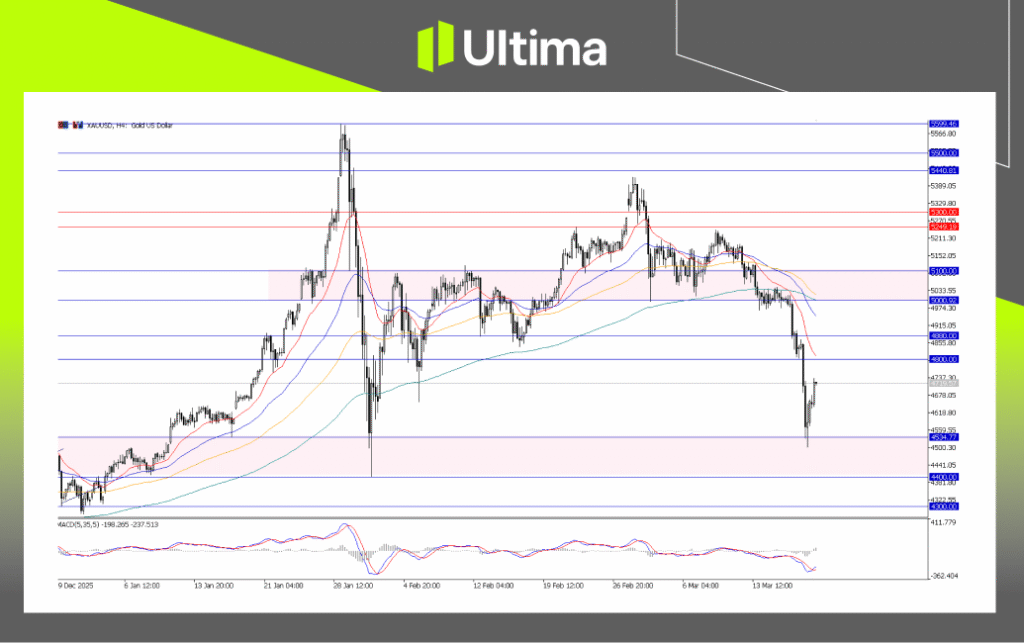

XAUUSD, H4 Chart | Ultima Markets MT5

From a technical perspective, Gold has developed a clear bearish reversal pattern. While the $4,500 level serves as a major structural support floor, upside momentum appears strictly limited.

The combination of a strengthening US Dollar and rising yields acts as a heavy lid on the market, particularly with the $5,000 handle now acting as formidable resistance. While Gold remains a preferred asset for hedging geopolitical tail risks, its near-term price appreciation is effectively capped by the current macroeconomic landscape.

2. Central Bank Pivot Trouble Equities

On the other hand, the convergence of energy volatility, mounting inflation/stagflation risks, and high sovereign yields is creating a massive fundamental headwind for the global equities market.

With Brent crude sustained above $110, corporate margins are under direct threat. The market is beginning to price in a “margin compression” scenario where companies face higher input costs at the same time the Fed is cooling consumer demand.

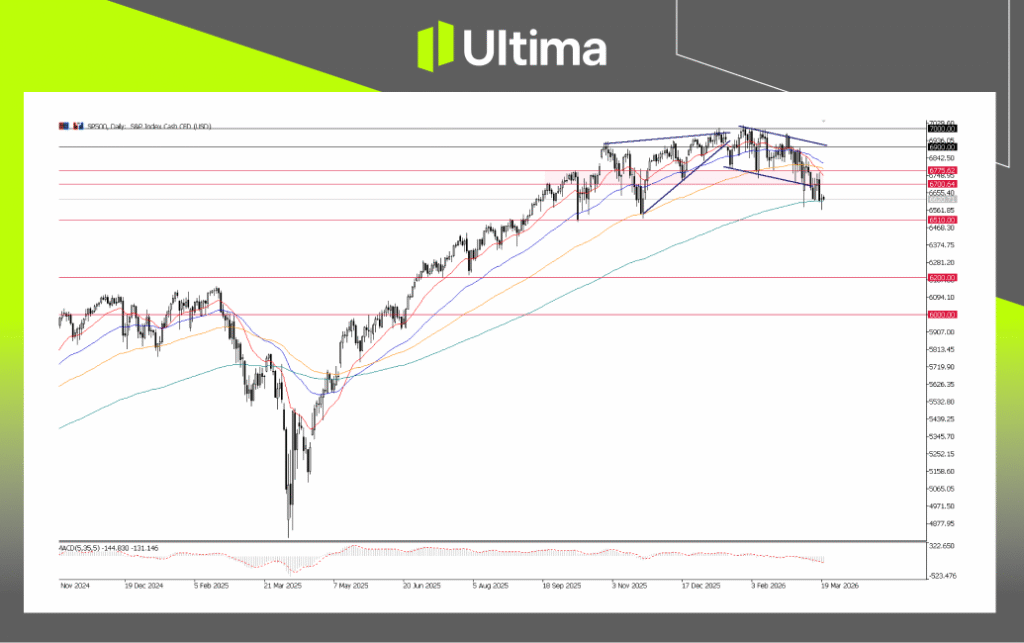

S&P500, Daily Chart | Ultima markets MT5

The technical landscape for the S&P 500 suggests a shift from a “buy-the-dip” regime to a defensive posture. In the coming weeks, expect the index to test lower liquidity pockets as it recalibrates to a world where interest rate cuts have been officially shelved.

Conclusion: The Defensive April Strategy

The “Hawkish Hold” has fundamentally changed the rules of engagement. As we enter April, the focus shifts from “chasing growth” to “preserving capital.”

Summary of Outlook:

Equities: Cautious/Bearish. Watch the 200-day SMA on the S&P 500.

Gold: Bearish near-term. Monitor the $4,500 support level.

Yields: Bullish. Expect the “Higher for Longer” narrative to drive volatility.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.