Important Information

This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

- You will not be guaranteed Negative Balance Protection

- You will not be protected by FCA’s leverage restrictions

- You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

- You will not be protected by Financial Services Compensation Scheme (FSCS)

- Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

- 1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

- 2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

- 3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

- 4.Investing through this website does not grant you the protections provided by the FCA.

- 5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

I confirm my intention to proceed and enter this website Please direct me to the website operated by Ultima Markets , regulated by the FCA in the United Kingdom

Ultima Markets App

Trade Anytime, Anywhere

What Is Volmageddon? How Does it Work?

Volmageddon is the nickname traders gave to the volatility shock on 5 February 2018. On that day, markets did not simply fall and recover in a typical risk off move. Volatility surged so sharply that popular short volatility products collapsed, and the mechanics behind those products appeared to spill over into the broader stock market.

If you have ever wondered why options trading often gets blamed whenever markets feel jumpy, Volmageddon is the clearest modern example. It shows how hedging, rebalancing, and crowded positioning can turn an ordinary sell off into a self reinforcing feedback loop.

What Volmageddon Means

Volmageddon refers to a sudden and extreme spike in equity volatility that triggers forced rebalancing in volatility linked strategies. In plain terms, it is when volatility rises so quickly that products and traders positioned for calm markets are forced to reduce risk and buy protection at the same time.

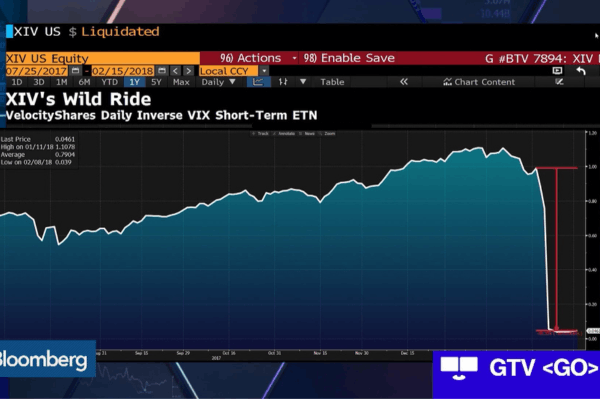

The headline number explains why the term stuck. On 5 February 2018, the VIX jumped more than 20 points, rising from 17.31 to 37.32, a 115 percent increase in a single session.

This move was unusually large relative to the equity decline, and official analysis suggested the surge was driven largely by internal dynamics in options and VIX related markets rather than only a change in long term expectations.

What Happened During Volmageddon in 2018

In the years leading up to Volmageddon, volatility was low and stocks generally trended higher. That environment made short volatility strategies attractive. Some traders sold volatility directly through derivatives. Others used exchange traded products designed to rise when volatility fell.

When a market stays calm for a long time, it is easy for short volatility exposure to become crowded. The risk is not obvious day to day because small moves do not punish the strategy. The problem is that the losses can become non linear when volatility spikes.

The Core Mechanism Behind Volmageddon

Markets often stabilise themselves. When prices drop, many investors step in, viewing lower prices as an opportunity. That buying pressure can slow the decline. Markets become unstable when falling prices create forced sellers. In that case, selling pressure feeds on itself.

Volmageddon is a textbook example of this idea. As volatility rose, short volatility positions lost value quickly. When losses accelerate, traders and products are forced to hedge, reduce exposure, or rebalance. Those actions can create additional demand for volatility related instruments, and can intensify stress in the underlying equity market.

Why The Market Close Became A Pressure Point

Timing mattered during Volmageddon. Many volatility linked products and strategies rebalance around predictable windows, often near the market close. When volatility is already rising, those flows can concentrate into a short period, adding momentum rather than reducing it.

Regulatory analysis captured this late session dynamic in a very concrete way. The AMF noted that in the last three minutes before VIX futures trading closed, close to 35,000 VIX futures contracts traded, and the S&P futures fell a further 0.7 percent over the same window. When many participants need to execute similar trades into thinner liquidity, even a short period can produce outsized moves.

The Role Of Short Volatility Products

Volmageddon is closely associated with short volatility exchange traded products, especially those tied to VIX futures. These products were popular because they performed well in calm markets. But their structure meant they could face extreme stress when volatility surged.

Research and post event analysis noted that short volatility ETPs suffered catastrophic losses in a single day, which is why the episode entered trading history. The broader lesson is that daily reset behaviour and embedded leverage can behave in ways that are not intuitive. A product can look stable for months, then a single extreme session dominates the outcome.

A Hidden Layer In The Story Data And Pricing Confusion

Fast markets also expose operational and data weaknesses. In the aftermath of Volmageddon, attention turned to how published index values behaved during the most chaotic window. The SEC later charged S&P Dow Jones Indices over failures related to an undisclosed quality control feature that caused certain index values to remain static during part of 5 February 2018.

This detail is not the core cause of Volmageddon, but it reinforces a practical message. In extreme conditions, not only do markets move fast, but the information traders rely on can become harder to interpret precisely when clarity is most needed.

Why Volmageddon Is Tied To Options Trading

Volmageddon is often explained through VIX products, but the VIX itself is rooted in options. It is derived from S&P 500 option prices and reflects both expected volatility and a volatility risk premium.

That link matters because options create a bridge between derivatives and the underlying market. Market makers who sell options often hedge their risk by trading the underlying index or futures. When hedging is stabilising, it can dampen moves. When hedging becomes forced, it can amplify them. This is why official analysis described Volmageddon as being driven largely by internal dynamics in equity options or VIX futures markets.

0DTE Options And The Volmageddon 2.0 Debate

The rise of 0DTE options has revived the Volmageddon conversation because these contracts can concentrate risk into very short timeframes. A 0DTE option expires the same day. That means its sensitivity to price moves can change rapidly during the session, which can increase the need for hedging adjustments.

JPMorgan has estimated that the daily notional value of 0DTE trading is close to one trillion dollars, which is why some strategists have warned about a potential Volmageddon 2.0 scenario. The key is not that option buyers themselves are systemically dangerous. The key is the hedging link created by dealers and market makers who take the other side.

How 0DTE Can Amplify Intraday Moves

The key concept is gamma. If dealers are positioned so that they are short gamma, their hedging can become pro cyclical. They may hedge by selling as the market falls and buying as it rises, which can amplify swings.

Cboe research finds that market maker gamma is often positive on average, which tends to reduce volatility, but it can flip negative, and volatility is elevated in those periods. This is why 0DTE can be stabilising in some sessions and destabilising in others. It depends on positioning and the direction of hedging flows.

Why 0DTE Does Not Automatically Mean Instability

It is also important not to confuse gross activity with net pressure. Cboe analysis suggests that net market maker hedging related to 0DTE can be small compared with overall liquidity, and that most SPX 0DTE activity is structured as limited risk positions such as long options or spreads.

In other words, the existence of heavy 0DTE volume does not automatically mean the market is fragile. The risk is more specific. It is one sided positioning combined with a shock that forces a large group of hedgers to act at the same time.

What Traders Can Learn From Volmageddon

Volmageddon is a case study in how market structure can shape outcomes. The first lesson is to understand whether you are short volatility, even indirectly. Many strategies that feel steady in calm markets can suffer when volatility rises quickly.

The second lesson is to respect products and strategies with daily reset mechanics or embedded leverage. These structures can behave in a non linear way, turning a single extreme day into a defining event.

The third lesson is to watch liquidity windows. When flows concentrate near the close or around key hedging times, moves can accelerate. Volmageddon showed how fast those accelerations can happen when many participants share similar exposures.

Finally, treat crowding as a risk factor by itself. When too many participants depend on the same assumption, such as volatility staying low, a reversal can become disorderly.

Conclusion

Volmageddon was not only a dramatic volatility spike. Volmageddon showed how crowded short volatility trades and mechanical hedging can turn a sell off into a feedback loop. As 0DTE options continue to grow, the core lesson remains the same. Markets become fragile when positioning is one sided and hedging becomes forced.

FAQs

Volmageddon is the February 2018 volatility shock when the VIX surged and short volatility products suffered rapid and severe losses.

Options trading did not cause Volmageddon on its own, but options and volatility linked hedging helped transmit stress through market structure during the event.

0DTE options do not automatically create instability, but if positioning becomes one sided and hedging turns pro cyclical, they could amplify intraday swings during a sharp shock.

Disclaimer: This content is provided for informational purposes only and does not constitute, and should not be construed as, financial, investment, or other professional advice. No statement or opinion contained here in should be considered a recommendation by Ultima Markets or the author regarding any specific investment product, strategy, or transaction. Readers are advised not to rely solely on this material when making investment decisions and should seek independent advice where appropriate.

Latest Articles

FOLLOW US

Ultima Markets is a member of The Financial Commission, an international independent body responsible for resolving disputes in the Forex and CFD markets.

All clients of Ultima Markets are protected under insurance coverage provided by Willis Towers Watson (WTW), a global insurance brokerage established in 1828, with claims eligibility up to US$1,000,000 per account.

Ultima Markets is the first United CFD broker to be part of the United Nations Global Compact.

FOLLOW US

TRADE WITH US

RISK DISCLOSURE

Risk Warning:

Trading leveraged financial products, including Contracts for Difference (CFDs), carries a high level of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors and should only be traded with funds you can afford to lose. You do not own or have any rights to the underlying assets of these derivatives (e.g., entitlement to dividends). Please ensure you fully understand the associated risks. Before trading, consider your level of experience, investment objectives, and seek independent financial advice if necessary. Refer to our legal documents and disclosures before making any trading decisions.

General Advice Warning:

The information provided on this website is general in nature and does not take into account your personal objectives, financial situation, or needs. Before acting on any advice, you should assess its appropriateness in light of your individual circumstances and consult our legal documentation.

Regional Restrictions:

The information and services on this website are not intended for residents of certain jurisdictions, including but not limited to the United States, United Kingdom, Singapore, and any jurisdictions subject to international sanctions. For further information, please contact our customer support team.

Regulatory Information:

Ultima Markets is a trading name shared amongst multiple entities operating in various jurisdictions. These following entities are authorised to operate under the Ultima Markets brand and trademarks.

-

Ultima Markets UK Limited, reference number 470325, is authorised and regulated by the Financial Conduct Authority (FCA). Registered address: 1 Blossom Yard, Fourth Floor, London, E1 6RS, UNITED KINGDOM.

-

Ultima Markets Ltd is authorised and regulated by the Financial Services Commission (FSC) of Mauritius as a Full-Service Investment Dealer (excluding Underwriting), under licence number GB 23201593.

Registered address: 2nd Floor, The Catalyst, 40 Silicon Avenue, Ebene Cybercity, 72201, Mauritius.

-

Ultima Markets EU OÜ, incorporated in Estonia with registry code 17134727. Registered address: Harju maakond, Tallinn, Kristiine linnaosa, Seebi tn 1-1501, 11316. This entity does not offer regulated financial products or provide trading services.

Copyright © 2026 Ultima Markets Ltd. All rights reserved.

-

Messenger

Continue on Messenger

Take the conversation to your Messenger account. You can return anytime.

Scan the QR code and then send the message that appears in your Messenger.

Open Messenger on this device.

-

Instagram

Continue on Instagram

Take the conversation to your Instagram account. You can return anytime.

Scan the QR code to open Instagram. Follow @ultima_markets to send a DM.

Open Instagram on this device.

-

Live Chat

-