This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

When the Strait of Hormuz reopens, analysts predict a price dip, but oil prices may remain 26% above pre-war levels due to lingering geopolitical risks.

The reopening of the Strait of Hormuz has eased immediate supply fears in global oil markets, but it has not brought prices back to normal. Brent crude has pulled back from recent highs, yet remains around 25–30% higher year-to-date.

What the market is now pricing is no longer a supply shock, but a geopolitical risk premium that is still embedded in energy prices. At the same time, sectors such as aviation, oil tankers, and shipbuilding are beginning to show clear second-order winners, while gold remains supported as a hedge against lingering uncertainty.

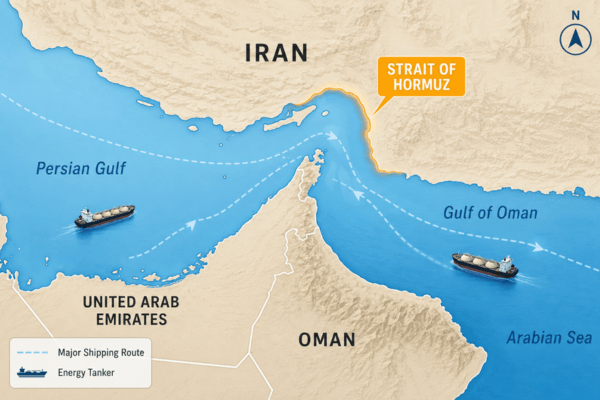

From Blockade to Reopening

The Strait of Hormuz, one of the most important oil transit routes in the world, has reopened following a US-Iran interim agreement that triggered a phased de-escalation of tensions in the region.

According to Bloomberg reporting on June 19, 2026, the US has formally ended its blockade, allowing commercial shipping to resume while broader negotiations over Iran’s nuclear programme continue under a 60-day framework.

Image Source: Ariana News

A Rapid Shift in Market Sentiment

US Vice President JD Vance confirmed that tanker traffic is already flowing again, with vessels carrying millions of barrels of crude observed moving through the Strait shortly after the announcement.

The immediate message to markets was clear: physical supply is returning, but political uncertainty is not fully resolved.

How Oil Price Reacted

Oil markets reacted quickly to the reopening.

During the height of the disruption, Brent crude briefly spiked toward the $95–$120 range as traders priced in worst-case supply scenarios. As the situation stabilised, prices corrected sharply, with Brent recently trading back below $80 per barrel.

However, the decline has not erased the broader trend.

Even after the pullback, oil remains roughly 30% higher year-to-date, reflecting how much risk premium had been embedded into pricing during the crisis period.

What matters now is not whether oil falls further, but where it stabilises. The market has removed panic, but not uncertainty.

Analyst Oil Price Projections Post Strait Reopening

As the market shifts from crisis pricing to negotiation-driven pricing, major institutions have maintained relatively tight but elevated forecasts for Brent crude.

The consensus suggests oil is no longer in a breakout phase, but instead operating within a structurally higher trading band.

Institution

Brent Crude Forecast

Outlook Summary

U.S. EIA

~$90–$98 average (2026)

Gradual supply recovery, but risk premium remains embedded

International Energy Agency (IEA)

Peak ~$100–$115, easing later

Short-term volatility followed by stabilisation

Goldman Sachs

~$95–$105 range

Geopolitical risk still supports elevated pricing

OPEC+

~$90–$100 range

Tight supply management and controlled production adjustments

Market Consensus

~$85–$105 trading band

Structural floor higher due to uncertainty and inventory rebuilding

The key takeaway is that even after reopening, no major institution expects a full return to pre-crisis oil levels. Instead, forecasts cluster around a higher equilibrium range, reflecting both supply constraints and persistent geopolitical risk.

Oil Market Outlook After the Strait Reopening

Although the Strait of Hormuz is operational again, analysts broadly agree that oil markets are not returning to pre-crisis conditions in the near term.

There are 3 key reasons for this.

First, full restoration of shipping and logistics capacity will take time. Even after reopening, operational bottlenecks and insurance adjustments continue to affect flows.

Second, spare production capacity in key OPEC+ members remains limited, which keeps the system sensitive to any renewed disruption.

Third, and most importantly, the geopolitical risk premium has not disappeared. It has simply shifted from acute fear to ongoing uncertainty.

As a result, most forecasts continue to place Brent crude in a broad $85–$105 range through 2026.

Sector Impact and Market Positioning

The reopening of the Strait of Hormuz has created a clear redistribution of winners and losers across global markets.

Oil Tankers: Strongest Direct Beneficiary

One of the most immediate impacts is in the tanker market.

Goldman Sachs notes that the disruption previously removed a significant portion of effective shipping capacity from the system. With the Strait reopening, this imbalance is reversing, tightening available vessel supply once again.

Earnings expectations for very large crude carriers (VLCCs) have been sharply upgraded, with daily rates potentially rising toward $250,000 in the base case and even higher in more optimistic scenarios.

Chinese operators such as COSCO Shipping Energy Transportation are often cited as key beneficiaries of this shift.

Aviation: Fuel Cost Relief Supports Earnings

Airlines are among the clearest indirect winners.

Lower crude prices translate into reduced jet fuel costs, which directly improves operating margins. Goldman Sachs estimates earnings improvements of 16% to 26% for major carriers, with budget airlines seeing more modest gains.

Beyond fuel savings, stabilising oil prices also reduce hedging costs and improve demand visibility for global travel.

In some scenarios, analysts suggest that Asian airline equities could see significant upside if lower fuel prices persist into the second half of the year.

Shipbuilding: Medium-Term Structural Support

Shipbuilders are not immediate beneficiaries, but the medium-term outlook is improving.

As freight markets stabilise and visibility returns, shipping companies are more likely to place new orders. This supports shipyard backlogs and long-term revenue cycles.

While short-term earnings impact is limited, sentiment and order flow are expected to strengthen gradually.

Container Shipping: A More Cautious Picture

Container shipping presents a more balanced outlook.

The reopening of alternative routes, including potential normalisation of Suez Canal flows, increases global shipping capacity. This can relieve bottlenecks but may also weigh on freight rates.

Goldman Sachs remains cautious on the segment, noting that increased supply could pressure margins even as operational efficiency improves.

Gold Is Still Supported by Uncertainty, Not Panic

Unlike oil, gold has not reversed sharply after the geopolitical de-escalation.

Instead, it remains structurally supported.

The reason is simple: gold does not only react to crisis events, but to uncertainty duration. While immediate risk has declined, the 60-day negotiation framework between the US and Iran means the outcome is still unresolved.

As a result, gold continues to trade with a defensive tone, supported by central bank demand and ongoing hedging activity.

The current environment is less about panic buying, and more about persistent caution.

A Controlled but Fragile Market Outlook

The reopening of the Strait of Hormuz has not reset the oil market. It has reshaped it.

We are no longer in a shock-driven phase. Instead, the market is now in a negotiation-driven phase where prices are anchored by both supply recovery and political uncertainty.

This creates a more controlled environment, but not a stable one.

Oil is no longer reacting to immediate disruption risk, but it is still reacting to the possibility of future disruption.

Key Indicators to Watch

The next phase of market direction will depend on a few critical signals.

Traders are closely watching:

Weekly US EIA inventory trends

Tanker flow volumes through the Strait of Hormuz

Progress in US–Iran negotiations under the 60-day framework

OPEC+ production discipline

Freight and insurance cost adjustments

Jet fuel demand recovery

These data points will determine whether oil settles into the mid-$80s range or drifts back toward $100 levels.

Conclusion

The reopening of the Strait of Hormuz has removed the immediate threat to global oil supply, but it has not removed uncertainty from the market.

Oil prices have stabilised, but at a higher structural level than before the crisis. At the same time, second-order effects are becoming clearer, with aviation and tanker markets emerging as key beneficiaries, while gold continues to act as a hedge against unresolved geopolitical risk.

In short, the market is no longer reacting to a shutdown. It is now pricing a fragile reopening.

FAQs

What happens to oil when the Strait of Hormuz reopens?

Oil usually falls as supply fears ease, but prices can stay elevated if geopolitical risks remain.

How long does it take for oil supply to normalise?

Full recovery will take months. Analysts predict that oil supply may not return to pre-conflict levels until late 2026.

Which sectors might benefit from the Strait reopening?

Oil tankers, airlines, and shipbuilders tend to benefit most. Container shipping is more mixed.

Share Now

Disclaimer:This content is provided for informational purposes only and does not constitute, and should not be construed as, financial, investment, or other professional advice. No statement or opinion contained herein should be considered a recommendation by Ultima Markets or the author regarding any specific investment product, strategy, or transaction. Readers are advised not to rely solely on this material when making investment decisions and should seek independent advice where appropriate.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.