This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

PCE Inflation Elevated: What’s Next for Fed, the Dollar & Oil Markets?

PCE Inflation Elevated: What’s Next for Fed, the Dollar & Oil Markets?

The latest US Personal Consumption Expenditures (PCE) Price Index has confirmed what recent CPI data already suggested: inflation remains stubbornly elevated above market expectations. While this data solidifies the Federal Reserve’s hawkish monetary policy stance, the market’s reaction across currency and commodity assets has been surprisingly counterintuitive.

The dollar went down in a typical “sell-the-news” move, but could the greenback extend its downside? And how will energy prices and Middle East developments impact the broader market following this PCE release?

Here is an in-depth analysis of the current macroeconomic landscape, the unexpected drop in the US dollar, and what the easing of geopolitical tensions means for energy markets moving forward.

Post PCE Data: The “Higher for Longer” Reality

The core takeaway from the latest PCE print is that the Federal Reserve’s “higher for longer” narrative remains completely intact. Sticky inflation is now the absolute focal point not just for the US central bank, but for global central banks as well.

While the annualized rate shows a clear move upward, the monthly expansion has decelerated. This deceleration suggests that inflation momentum may be swinging away from its recent aggressive acceleration, largely because energy prices have started cooling off from their recent peaks.

Still, the underlying reality remains unchanged. Multiple Fed officials have recently emphasized their concern over the persistence of consumer price pressures, which have been heavily driven by the threat of energy-led inflation.

Because the data fails to show any significant or rapid cooling in core price pressures, the probability of the Fed cutting interest rates in 2026 has effectively been taken off the table. The market must now navigate a macro environment where restrictive monetary policy is the established baseline rather than a passing phase.

The US Dollar’s Counterintuitive Drop

Given the hawkish inflation data and the baseline expectation of sustained high interest rates, traditional economic theory dictates that the US dollar should have strengthened. Instead, the dollar dropped. This divergence can be attributed to two primary market catalysts:

A Classic “Sell-the-News” Event: The market is forward-looking and had already aggressively priced in the high inflation expectations and the Fed’s higher-for-longer policy. This anticipation caused the dollar to surge in the days leading up to the PCE release. Once the data merely confirmed what was already priced in, traders took profits, triggering a textbook sell-the-news pullback.

Fading Geopolitical Risk Premiums: The recent 60-day truce agreement between the US and Iran has injected a wave of optimism into the markets, raising hopes for a full peace resolution in the Middle East. As the immediate threat of conflict dissipates, the substantial risk premium that was baked into oil prices has faded. This drop in crude oil prices temporarily eases the underlying fear of a severe energy inflation shock, which in turn reduces safe-haven inflows into the dollar.

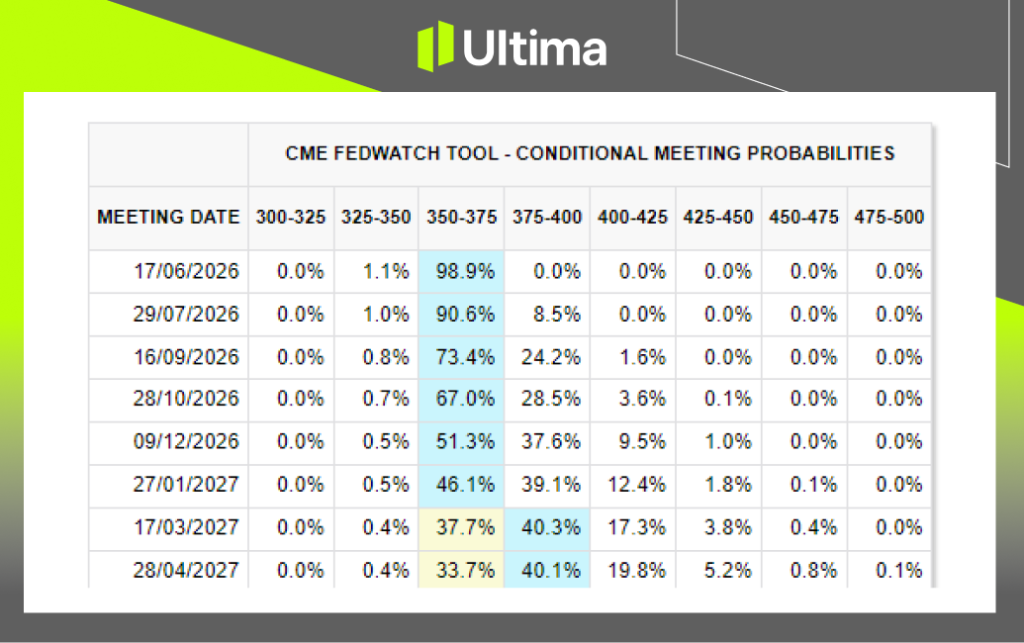

In fact, this de-escalation has actually priced out some of the extreme hawkish expectations surrounding the Fed. Previously, a growing segment of the market expected the Fed to hike rates once or twice in late 2026 or early 2027 to combat an energy-driven inflation shock. This view has seen a significant pushback, according to CME FedWatch data.

Fed Rate Probabilities | Source: CME Group

Market pricing now indicates a 51.3% probability that the target Federal Funds Rate will remain steady at 3.50% – 3.75% by the end of 2026. This marks a sharp reversal from just a week earlier, when more than 50% of market participants anticipated 1 to 2 additional rate hikes by late 2026 or early 2027.

The Long-Term Outlook: A Struggling Dollar

Turning our focus specifically back to the dollar, what can we expect moving forward?

When we strip away the temporary safe-haven demand generated by Middle East tensions and the immediate short-term repricing of Fed policy, the US dollar fundamentally lacks the structural momentum required for a sustained breakout.

USDX, Daily Chart | Ultima Markets MT5

Looking at the broader trend, the dollar index has struggled to find any strong fundamental catalyst to force a sustained surge past the critical 99 – 100 structural zone, a level it has continuously traded below over the past year.

The long-term macroeconomic outlook for the greenback remains heavily burdened by systemic structural headwinds. Most notable among these are the massive US government debt load being financed at historically high interest rates, and the ongoing, gradual global shift toward de-dollarization.

Furthermore, the dollar’s inability to break above 100 despite a highly hawkish Fed baseline signals that buyers are purely driven by short-term tactical plays rather than long-term structural confidence.

USDX, H4 Chart | Ultima Markets MT5

In the near term, the dollar will likely find it incredibly difficult to break above the 99 – 100 threshold. The immediate focus for traders should be shifted toward potential downside risks—or at the very least, treating upside moves with caution—specifically watching whether the 99 level will hold as a firm technical resistance ceiling.

If energy inflation fears continue to ease, the current hawkish foundation supporting the dollar will naturally erode, leaving it with very few bullish catalysts.

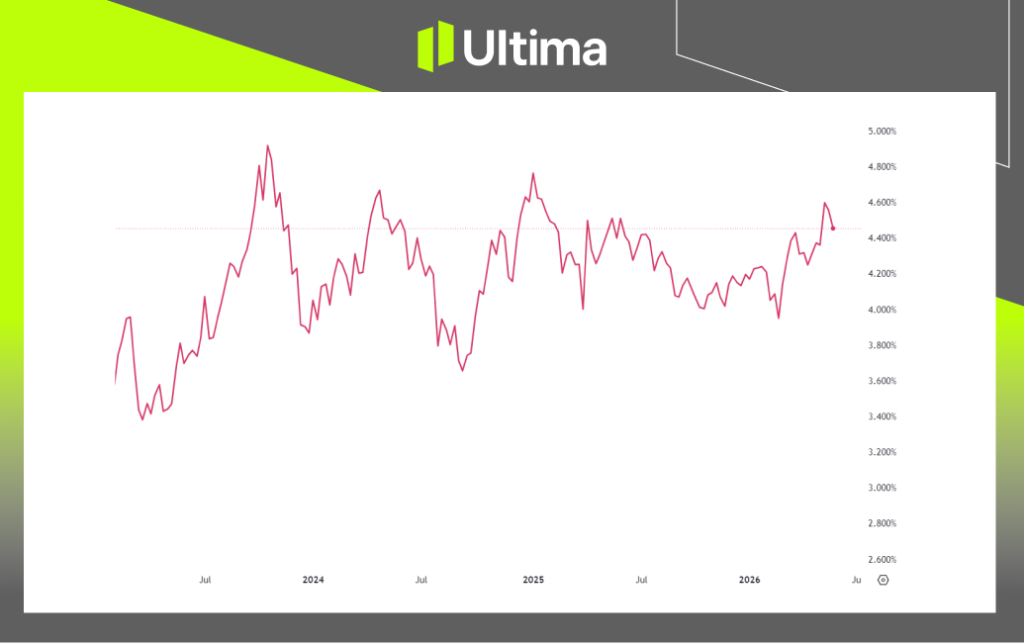

The Bond Market Corroborates the Move: Treasury Yields Retreat

The dynamics in the US fixed-income market perfectly mirror the US dollar’s counterintuitive drop. In the weeks leading up to the PCE release, the US 10-year Treasury yield surged to a 2026 high of 4.67%, heavily pricing in the energy inflation shock and the Fed’s hawkish shift.

US 10-Year Treasury Yield | Chart Source: Trading View

However, following the PCE data release and the announcement of the US-Iran truce, the 10-year yield has swiftly retreated back toward the 4.45% – 4.50% range. This confirms that the bond market, much like the currency market, had already fully digested the “higher for longer” scenario.

As Treasury yields pull back from their extreme peaks, the interest rate differential advantage that typically fuels dollar buying has stalled. Traders should continue to closely monitor the trajectory of Treasury yields; if yields continue their downward trend, it will apply further technical downside pressure on the greenback.

Oil Markets: A “Sell the Rally” Opportunity

The dynamics in the crude oil market are shifting rapidly. With the US-Iran truce successfully de-escalating regional tensions, energy inflation fears are subsiding.

On a side note, this adds another unfavorable macro factor for the dollar: as the oil market Eases, inflation expectations will likely slow down, depriving the dollar of an aggressively hawkish Fed narrative.

Turning back to oil, we expect that crude prices have established a definitive cyclical top under these current conditions. Because market sentiment is heavily leaning toward geopolitical relief in the Middle East, the path of least resistance for oil is structurally lower.

Barring any sudden and significant military re-escalation during the truce, any upward bounce or technical rebound in oil prices should be viewed strategically as a classic “sell the rally” opportunity.

UKOUSD, H4 Chart | Ultima markets MT5

Looking at the technicals of UKOUSD (Brent), the global benchmark is trading at the lower boundary of the broad consolidation range established since the geopolitical breakout on February 28th. Furthermore, Brent is on track to close with a strong bearish candle for June, signaling that the energy market is systematically pricing out the geopolitical premium.

Expect oil prices to continue to slowly ease in the coming weeks and months, provided no fresh escalation shocks disrupt the Middle East landscape during this 60-day truce window.

Summary: A Persistent Hawkish Baseline, But Flawed Long-Term Catalysts

To summarize, while the elevated PCE data guarantees that the Federal Reserve will maintain its hawkish posture, the policy narrative is no longer an unconditional driver of multi-year dollar strength.

The baseline expectation has definitively shifted: the “higher-for-longer” landscape effectively removes any realistic chance of a Fed rate cut in 2026. However, this hawkish stance does not automatically translate into a license to hike. For the central bank to actively tighten monetary policy again, it would require a severe, prolonged energy inflation shock—a risk that is rapidly diminishing.

Without a sustained resurgence in crude oil, the primary catalyst that previously supercharged the dollar’s upward momentum is fading. Consequently, unless geopolitical hostilities face a sudden and severe re-escalation, crude oil is highly unlikely to achieve new highs. For traders, this leaves the greenback caught in a structural squeeze: fundamentally supported by high short-term yields, yet technically capped and devoid of the structural, long-term catalysts needed to ignite a true bullish breakout.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.