This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

The Fed’s Dramatic Pivot! A Deep Dive into the FOMC Minutes

The Fed’s Dramatic Pivot! A Deep Dive into the FOMC Minutes

The Hawkish Reversal From “Delaying Rate Cuts” to “Preparing to Hike”

How much can the world’s most influential central bank shift its stance in just one month? A close comparison of the FOMC’s March and April 2026 meeting minutes reveals that the rate-cut party markets had been eagerly anticipating has not only been called off — policymakers at the highest levels have now sunk into deep anxiety over rekindling inflation. From “mild defense” to “hawkish war footing,” the details of this sweeping attitude reversal are buried in the lines of the minutes.

Outlook and Current Conditions

When it came to Outlook and Current Conditions, the gap between March and April was stark. In March, most committee members remained relatively optimistic, viewing elevated inflation as merely a short-term disturbance from tariff effects and the early stages of the Middle East conflict. Their greater concern at the time was actually the labor market, where they warned conditions were fragile and “vulnerable to adverse shocks” — even worrying this could “push the unemployment rate sharply higher.”

By April, however, incoming economic data had shattered that optimism entirely. Committee members were alarmed to find that core inflation had not cooled at all; rather, it had “moved further above 2 percent.” Elevated oil prices were rapidly experiencing spillover effects, pushing up costs across transportation, airfares, and even the technology and software sectors. What unnerved officials even more was their growing concern that a prolonged period of high inflation could alter the pricing and wage-setting behavior of businesses and workers alike, ultimately leading to the de-anchoring of inflation expectations.

The April minutes also specifically highlighted the severe pressure that high prices were placing on “lower-income households,” and added extensive new discussion of financial stability risks — including concerns about AI disrupting business models and triggering a wave of withdrawals from Private Credit markets, as well as the dangers of high leverage among hedge funds. After confirming that recent sluggish job growth was actually consistent with a slowdown in labor force expansion and that the labor market “suggested stabilization,” the FOMC’s policy focus shifted entirely back to fighting inflation. Most strikingly, while the March meeting had only discussed delaying rate cuts, by April “A majority” of members had explicitly stated that if inflation remained persistently above target, “policy firming would be appropriate.” This signals that rate hikes have formally re-entered the Fed’s list of live options.

Committee Policy Actions

This anxiety over broadening inflation immediately triggered a rare internal fracture during the Committee Policy Actions phase. In March, the committee had achieved broad consensus — the lone dissenter being dovish member Stephen I. Miran, who called for an immediate rate cut. The post-meeting statement at the time lightly described inflation as “somewhat elevated” and retained language about “considering the extent and timing of additional adjustments,” continuing to signal an easing bias to markets.

By April, however, the hawks struck back forcefully. First, the statement dropped “somewhat,” characterizing inflation simply as “elevated,” while explicitly warning that the Middle East situation was creating “a high level of uncertainty.” Even more eye-catching was the emergence of three new dissenters in the vote: Beth M. Hammack, Neel Kashkari, and Lorie K. Logan. These three hawkish heavyweights were not objecting to holding rates steady — they were vigorously protesting language in the post-meeting statement that still implied an expectation of future rate cuts. They forcefully demanded “a more two-sided characterization,” insisting that markets be made to understand that future monetary policy is no longer a one-way path toward cuts, and that rate hikes are equally on the table.

Conclusion

From the dovish defensiveness of March to the sweeping internal revolt openly pointing to possible rate hikes in April, the FOMC has decisively broken free from the one-directional rate-cut mindset. Confronted with stubborn and spreading inflation, monetary policy is now entering an intense and treacherous phase of calculated, two-way maneuvering.

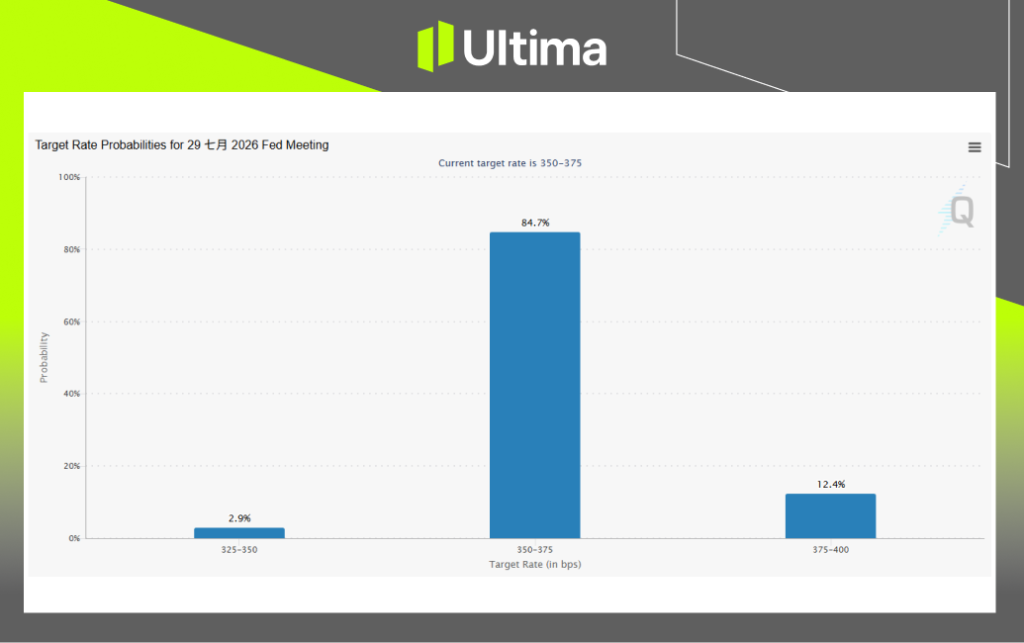

According to FedWatch, there is a greater than 95% probability that the FOMC will hold rates steady at its June meeting, while the July forecast shows a 12% probability of a rate hike.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.