This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Learn the usd to pkr forecast 2025–2030 with scenarios, key drivers, and trader tips, rates, ranges, SBP policy, reserves, and IMF milestones.

USD to PKR Forecast 2025

Expect interbank USD/PKR to trade mostly in the 276–290 range through 2025, with spot around ~282–284 today. The band is anchored by SBP’s 11% policy rate, rising FX reserves (SBP ~$14.47bn; total ~$19.69bn) and IMF progress; upside risks are oil and a stronger global USD.

Base Case (Highest Probability): 276–290

With 11% policy rate, improving reserves, and IMF continuity, we expect range-bound trading with two-way moves inside 276–290 as SBP leans against disorderly volatility while allowing data-led adjustment. Upside USD risk (weaker PKR) can re-emerge if oil spikes or the broad USD strengthens.

Bullish PKR Scenario (Stronger Rupee): 275–278

Requires softer inflation prints, steady remittances, on-time IMF disbursements, and a benign global USD backdrop.

Bearish PKR Scenario (Weaker Rupee): 285–295+

Could follow higher energy import costs, delays in external inflows, or a renewed global dollar rally. Watch Brent prices and SBP’s weekly reserve releases.

Monitoring Checklist

SBP close (daily): M2M USD/PKR and weighted bid/offer to see the previous day’s true interbank close and tightness.

Live boards (intraday): Check if spot is hugging the lower half (bullish PKR) or upper half (bearish PKR) of our band.

IMF pipeline (newsflow): SLA to Board approval to disbursement, each step lowers risk premia. Inflation prints & MPS (monthly/8-weekly): If CPI cools and policy credibility holds, lean to 275–278 tests; if CPI re-accelerates, keep powder dry near 288–292.

Remittances (monthly): Strong inflows often support PKR around reporting dates.

Key Takeaways

Spot: Interbank reference around PKR 281 per USD (late Oct). Open-market quotes vary by counterparty and spread.

Policy backdrop: SBP policy rate 11%, with the Bank signalling caution as headline inflation moved higher in September.

Macro cushion: Reserves improved (SBP ~$14.47bn; total ~$19.69bn), aided by IMF progress (staff-level agreement, Oct 14).

Baseline 1–3 months: Range-bound bias PKR 276–290 barring shocks, as tight real rates, reserves, and IMF pipeline temper volatility; upside USD risk if energy prices or USD strength re-accelerate. (Reasoned view synthesising the data below.)

6–12 months: Direction hinges on inflation trend, fiscal execution under IMF, energy imports, and global USD. Sustained reform + stable commodity prices favor gradual PKR stabilization; slippage or external shocks risk PKR depreciation bursts.

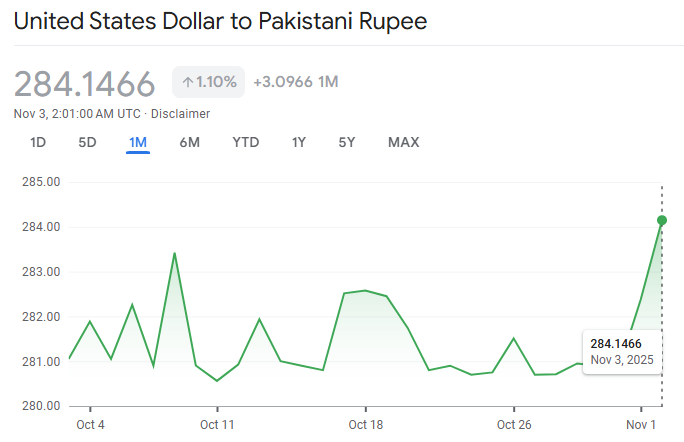

Current Pakistani Rupee Price Performance

The chart shows USD/PKR at 284.1466 on Nov 3, 2025, up +1.10% month-on-month (+3.0966 PKR). For most of October the pair was range-bound around 281–282, with a brief mid-month dip just below 281 and a modest bounce toward ~283 in the third week.

After late-October softness near ~281, early November saw a sharp upswing that pushed USD/PKR to the month’s high around 284.1. In plain terms, the rupee was broadly stable through October and then weakened at the turn of the month. For users tracking a usd to pkr forecast, this chart suggests a tight trading band for most of the month with a late break higher, placing the focus on upcoming policy signals, reserves data, and global USD moves to confirm whether this pop sustains or fades back into the earlier range.

What Will Move USD/PKR in 2025

Monetary policy & real rates: Holding at 11% keeps real rates positive, PKR supportive if inflation stays contained.

External financing: An active IMF program supports confidence and reserves; slippage would pressure PKR

Reserves management: Higher SBP reserves (~US$14.5bn) provide room to smooth volatility in a managed float.

Global USD & oil: A stronger broad USD and costlier oil typically weaken PKR via the import bill and risk sentiment.

Seasonality: Import cycles and remittance peaks can tilt short-term USD demand.

USD to PKR Forecast 2030

By 2030, a realistic usd to pkr forecast is a gradual depreciation path (not a straight line), with the base case guided by Pakistan maintaining IMF-backed reforms, positive real rates, and adequate reserves, while shocks (oil, global USD, policy slippage) could push the rupee into step-downs rather than a single smooth trend.

1) Reform-Led Stabilization (Constructive Base Case)

Assumptions: SBP preserves policy credibility (positive real rates), IMF reviews stay on track (board approvals and timely disbursements), and reserves trend higher from current levels; remittances remain firm.

FX implication: Slow, trend depreciation broadly in line with the inflation gap vs. the U.S., punctuated by multi-month stable stretches if reserves are rebuilt and current-account gaps stay small. (SBP projects low current-account deficits and rising reserves into 2026, a helpful starting point.)

Risk checks: If CPI stays contained and IMF milestones are met, the rupee tends to avoid crisis-style moves.

2) Stop-Go Reform with External Shocks

Assumptions: Intermittent reform progress; occasional oil spikes and bouts of stronger global USD; reserves still manageable but not rising consistently.

FX implication: Step-wise depreciations (one-off re-pricings) followed by stabilization bands.

Risk checks: Watch for reserves that stall or decline and wider interbank bid/offer spreads around stressful weeks.

3) Policy Slippage (Bearish Tail)

Assumptions: Delays in IMF reviews/disbursements, weak fiscal delivery, persistent energy/import pressures.

FX implication: Faster depreciation with volatility clusters, potentially requiring tighter policy or administrative measures to re-anchor expectations.

Pakistan is presently under EFF/RSF with a fresh staff-level agreement in Oct 2025, and the SBP policy rate is 11%, a restrictive, PKR-supportive starting point. Whether these supports persist determines where 2030 lands within the range of outcomes.

Conclusion

USD/PKR spent most of October in a tight 281–283 band before a quick pop to ~284 in early November, consistent with our 2025 base range of 276–290. For forex traders, the playbook is simple: let SBP policy (11%), reserves, CPI prints, and IMF milestones guide bias; scale into positions in tranches near band edges; and protect downside with clear stop levels and size limits.

If you’re ready to act on this view, trade USD/PKR on Ultima Markets with real-time pricing, an economic calendar for SBP/IMF events, and tools for risk control (price alerts, pending orders, and hedging via staged entries). Prefer to practice first? Start with a demo account and pressure-test your plan before going live.

Share Now

Disclaimer:This content is provided for informational purposes only and does not constitute, and should not be construed as, financial, investment, or other professional advice. No statement or opinion contained herein should be considered a recommendation by Ultima Markets or the author regarding any specific investment product, strategy, or transaction. Readers are advised not to rely solely on this material when making investment decisions and should seek independent advice where appropriate.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.