This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Rate Differentials in Focus: What Fed Cuts and BOJ Normalization Mean for USD/JPY?

23 September 2025

The Federal Reserve’s latest rate cut marks the start of a new easing cycle, while the Bank of Japan held rates but hinted at gradual normalization through balance-sheet adjustments. This evolving policy divergence is narrowing the U.S.–Japan rate gap, a key driver of USD/JPY.

Depending on how the Fed’s pace of easing aligns with the BOJ’s next moves and shifts in global risk sentiment, USD/JPY could face downside pressure, remain range-bound, or even resume higher.

Fed Signals a New Easing Cycle

On September 18, 2025, the Federal Reserve lowered its policy rate by 25 basis points, bringing the federal funds target range down to 4.00%–4.25% — its first adjustment since December. The move was framed as a “risk management” step, with Chair Jerome Powell highlighting signs of slowing job growth and mounting unemployment pressures.

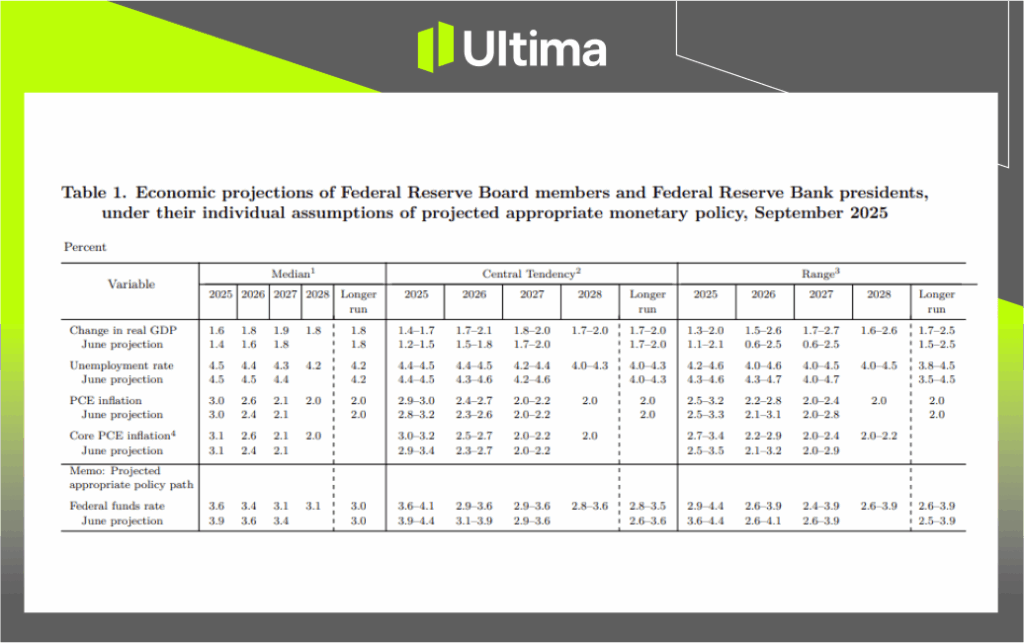

In its September Summary of Economic Projections (SEP), the Fed downgraded 2025 GDP growth to 1.6% from 1.9%, reflecting weaker consumer spending and softer business investment. The unemployment rate is now expected to rise to 4.6% by year-end, compared with 4.3% in June.

SEP | Source: Federal Reserve

On inflation, officials project both headline and core PCE holding around 3.0–3.1% in 2025, before gradually converging toward the 2% target by 2026–2027. Powell acknowledged that tariffs remain a headwind but stressed they appear to be “more one-off than persistent.”

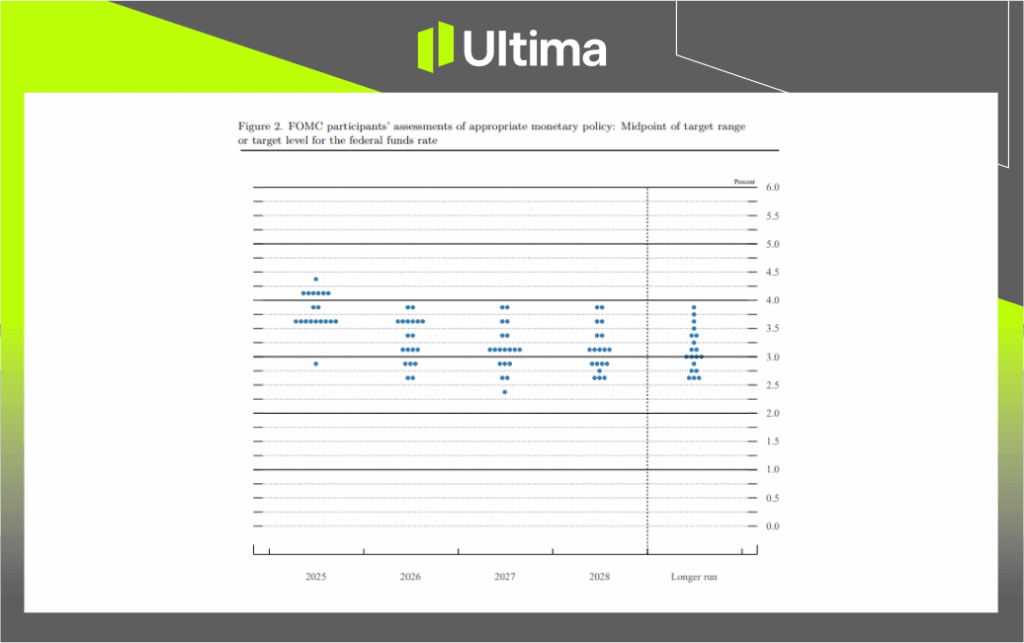

Fed Dot Plot in September | Source: Federal Reserve

The updated dot plot signaled a clear bias toward further easing, with two more cuts likely in the final two meetings of 2025. At the same time, policymakers emphasized a data-dependent stance, keeping the option open for additional action if labor market weakness deepens further.

This effectively marks the start of a new easing cycle, even as inflation remains elevated near 3% — above the Fed’s long-term 2% target. The decision underscores a shift in tolerance toward above-target inflation in the post-pandemic environment, where labor market stability and growth risks are now taking precedence.

In short, unless inflation surprises to the upside with a sharp surge beyond 3%, the Fed has formally pivoted into a new round of easing following its September 2025 meeting.

BOJ: Holding Steady, Hinting at Change

One day later, the Bank of Japan kept its policy rate unchanged at 0.50%, but the decision carried a hawkish undertone. Two board members — Hajime Takata and Naoki Tamura — dissented, calling for an immediate hike to 0.75%. The split underscores growing internal pressure for tighter policy.

More significantly, the BOJ unveiled its first concrete step toward balance-sheet normalization: it will begin the gradual sale of ETFs and J-REITs, at a pace of about ¥330 billion per year in ETFs and ¥5 billion per year in REITs. While modest, the move marks a symbolic shift after years of extraordinary monetary easing.

The Rate Differential: Wide, but Risk of Compression

For now, the U.S.–Japan policy rate spread remains wide. With the Fed’s midpoint at 4.125% and the BOJ at 0.50%, the nominal gap stands at roughly 362 basis points. This differential has underpinned persistent yen weakness and the attractiveness of carry trades.

But markets look ahead — and the risk is that this spread begins to compress:

If the Fed follows through with another 50–75 bps of cuts over the next six months, U.S. front-end yields will fall further.

If the BOJ moves beyond asset sales and delivers even a modest hike, Japanese yields will rise.

Such a combination would erode the carry advantage supporting long USD/JPY positions, creating conditions for potential yen appreciation.

Market Implications for USD/JPY

While recent developments create conditions for potential yen appreciation, the lack of a firm policy commitment from the BOJ and lingering domestic uncertainties in Japan have limited follow-through. Investors remain cautious, with USD/JPY showing resilience despite the hawkish undertone in the BOJ’s latest outlook.

Looking ahead, the trajectory of USD/JPY will hinge on the interaction between monetary policy paths and global risk sentiment:

Base Case (Gradual Spread Compression): If the Fed cuts ease further while the BOJ normalizes further, USD/JPY is likely to drift lower, with downside moves in the next quarter could be on the table as carry trades unwind in stages.

Risk-Off Shock: Should Fed cuts be interpreted as a signal of recession risk, safe-haven demand for yen could trigger a sharper, disorderly move lower in USD/JPY.

Status Quo Extended: If the BOJ stalls on hikes and sticks only to balance-sheet adjustments, while the Fed limits itself to one or two cuts, the differential remains wide and USD/JPY may stabilize or even resume higher in risk-on conditions.

USDJPY Outlook: Range Bound Set to Breakout

USD/JPY, Daily Chart | Source: Ultima Market MT5

USD/JPY has been consolidating in a tight range for nearly two months, reflecting investor indecision amid diverging Fed and BOJ policy expectations. The pair continues to fluctuate between key support and resistance zones, with momentum indicators suggesting a potential breakout ahead.

Key Resistance Levels: 148.00 remains the immediate barrier, with 149.00 as the next level. A sustained break above 149.00 could open the path toward the psychological 150.00 level.

Key Support Levels: Immediate support lies at 146.80, followed by the critical 146.00 level. A decisive drop below 146.00 would confirm a bearish breakout, exposing downside risks toward 142.00 or further.

The prolonged range suggests that USD/JPY is primed for volatility.

Analyst View

The Fed and the BOJ are currently moving in opposite directions: the Fed signaling an easing cycle while the BOJ cautiously explores normalization. Although the absolute policy gap still favors the U.S. Dollar, the shift in direction suggests the potential for eventual yen strength, particularly when considering narrowing rate differentials and the implications for carry trades.

That said, USD/JPY’s outlook cannot be judged by monetary policy alone—broader macro drivers such as global risk sentiment, U.S. yields, and capital flows will also play critical roles. At this stage, a gradual narrowing of the rate differential could provide incremental support for the yen, but confirmation will depend on upcoming data and central bank signals.

Ultimately, price action remains the most direct gauge of market sentiment. Traders should watch closely for a decisive breakout from the prolonged consolidation, as this will likely define the next major trend for USD/JPY.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.