Ultima Markets App

Trade Anytime, Anywhere

Important Information

This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

- You will not be guaranteed Negative Balance Protection

- You will not be protected by FCA’s leverage restrictions

- You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

- You will not be protected by Financial Services Compensation Scheme (FSCS)

- Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: Ultima Markets is currently developing a dedicated website for UK clients and expects to onboard UK clients under FCA regulations in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

- 1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

- 2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

- 3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

- 4.Investing through this website does not grant you the protections provided by the FCA.

- 5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

I confirm my intention to proceed and enter this website Please direct me to the website operated by Ultima Markets , regulated by the FCA in the United Kingdom

What is the Sortino Ratio?

The Sortino Ratio is a risk-adjusted return metric that is used by investors and traders to assess an investment’s performance relative to its downside risk. Unlike the Sharpe Ratio, which penalizes both upside and downside volatility, the Sortino Ratio focuses specifically on downside risk, making it a more accurate measure of the risk-adjusted return for risk-averse investors.

Key Takeaway:

- The Sortino Ratio emphasizes downside volatility, which is the harmful part of price fluctuations.

- It helps investors evaluate whether an investment’s returns justify its risks, especially focusing on avoiding losses.

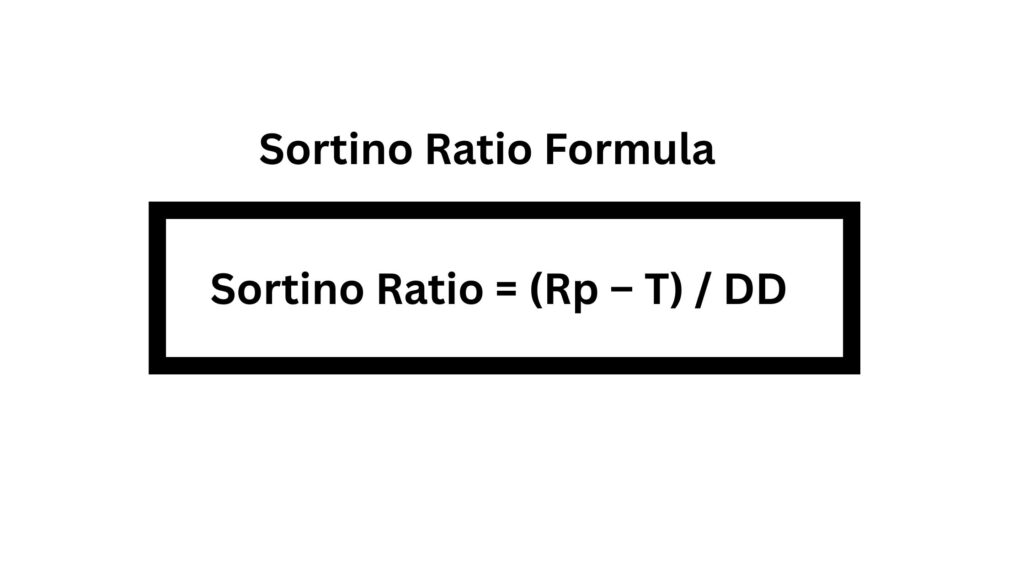

How to Calculate the Sortino Ratio

The formula to calculate the Sortino Ratio is straightforward but powerful. It involves comparing the investment’s actual return to a target return, usually the risk-free rate, and dividing that by the downside deviation.

Sortino Ratio Formula:

Sortino Ratio = (Rp – T) / DD

Where:

- Rp = Actual return of the portfolio

- T = Target or required rate of return (typically the risk-free rate)

- DD = Downside deviation (standard deviation of negative returns)

Example of the Sortino Ratio Formula

Let’s consider an investment scenario where:

- The annual return is 15%

- The risk-free rate is 5%

- The downside deviation is 10%

Using the Sortino Ratio formula, we calculate:

Sortino Ratio = (15% – 5%) / 10% = 1.0

This means that for every unit of downside risk, the investor has earned 1% in excess return.

What is a Good Sortino Ratio?

Generally, a Sortino Ratio greater than 1.0 is seen as a positive sign, indicating that the investment’s returns are outperforming the downside risks. Here’s a general guide to interpreting the Sortino Ratio:

- < 1.0: Below average risk-adjusted return, indicating high downside risk

- 1.0 – 2.0: Acceptable to good risk-adjusted return

- 2.0: Excellent risk-adjusted return, showing strong performance relative to downside risk

A Sortino Ratio above 2.0 typically indicates outstanding risk-adjusted returns.

Sortino Ratio Example: A Real-World Case

Let’s say you have a portfolio with:

- An annual return of 12%

- A target return of 4%

- A downside deviation of 8%

The Sortino Ratio would be:

Sortino Ratio = (12% – 4%) / 8% = 1.0

This tells you that the portfolio is achieving reasonable returns for the amount of downside risk involved.

Advantages and Limitations of the Sortino Ratio

Advantages:

- Focus on Downside Risk: The Sortino Ratio penalizes only the negative volatility (downside risk), making it a more accurate measure for risk-averse investors compared to the Sharpe Ratio.

- Better Risk Assessment: It helps in better understanding how much return is earned for each unit of downside risk.

- Improved Accuracy for Non-Normal Distributions: For assets with skewed returns, the Sortino Ratio provides a clearer picture of risk-adjusted performance.

Limitations:

- Historical Data Dependency: The ratio depends on historical data, and past performance might not always predict future returns.

- Subjectivity in Target Return: The choice of target return can affect the outcome, making it subjective to the investor’s expectations.

- Limited Use for Speculative Assets: For highly volatile or speculative assets, the Sortino Ratio might not fully capture the risks due to large upside volatility.

Conclusion

Understanding the Sortino Ratio is essential for any trader or investor who seeks to optimise their risk-adjusted returns. By focusing on downside risk, the Sortino Ratio provides a more accurate assessment of an investment’s performance, helping you make informed decisions while minimizing potential losses. Whether you’re assessing stocks, bonds, or forex, this ratio is a powerful tool for evaluating risk versus return.

At Ultima Markets, we provide a secure and transparent trading environment to support traders who want to optimise their strategies with the scalp trading strategy. By leveraging tools like the Sortino Ratio, we empower you to make smarter, data-driven decisions. Our platform, which is committed to sustainability and innovation, allows you to trade with confidence, knowing that your investments are backed by strong regulatory oversight and cutting-edge technology.

Disclaimer: This content is provided for informational purposes only and does not constitute, and should not be construed as, financial, investment, or other professional advice. No statement or opinion contained here in should be considered a recommendation by Ultima Markets or the author regarding any specific investment product, strategy, or transaction. Readers are advised not to rely solely on this material when making investment decisions and should seek independent advice where appropriate.

Latest Articles

FOLLOW US

Ultima Markets is a member of The Financial Commission, an international independent body responsible for resolving disputes in the Forex and CFD markets.

All clients of Ultima Markets are protected under insurance coverage provided by Willis Towers Watson (WTW), a global insurance brokerage established in 1828, with claims eligibility up to US$1,000,000 per account.

Ultima Markets is the first United CFD broker to be part of the United Nations Global Compact.

FOLLOW US

TRADE WITH US

RISK DISCLOSURE

Risk Warning:

Trading leveraged financial products, including Contracts for Difference (CFDs), carries a high level of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors and should only be traded with funds you can afford to lose. You do not own or have any rights to the underlying assets of these derivatives (e.g., entitlement to dividends). Please ensure you fully understand the associated risks. Before trading, consider your level of experience, investment objectives, and seek independent financial advice if necessary. Refer to our legal documents and disclosures before making any trading decisions.

General Advice Warning:

The information provided on this website is general in nature and does not take into account your personal objectives, financial situation, or needs. Before acting on any advice, you should assess its appropriateness in light of your individual circumstances and consult our legal documentation.

Regional Restrictions:

The information and services on this website are not intended for residents of certain jurisdictions, including but not limited to the United States, United Kingdom, Singapore, and any jurisdictions subject to international sanctions. For further information, please contact our customer support team.

Regulatory Information:

Ultima Markets is a trading name shared amongst multiple entities operating in various jurisdictions. These following entities are authorised to operate under the Ultima Markets brand and trademarks.

-

Ultima Markets UK Limited, reference number 470325, is authorised and regulated by the Financial Conduct Authority (FCA). Registered address: 1 Blossom Yard, Fourth Floor, London, E1 6RS, UNITED KINGDOM.

-

Ultima Markets Ltd is authorised and regulated by the Financial Services Commission (FSC) of Mauritius as a Full-Service Investment Dealer (excluding Underwriting), under licence number GB 23201593.

Registered address: 2nd Floor, The Catalyst, 40 Silicon Avenue, Ebene Cybercity, 72201, Mauritius.

Copyright © 2026 Ultima Markets Ltd. All rights reserved.

-

Messenger

Continue on Messenger

Take the conversation to your Messenger account. You can return anytime.

Scan the QR code and then send the message that appears in your Messenger.

Open Messenger on this device.

-

Instagram

Continue on Instagram

Take the conversation to your Instagram account. You can return anytime.

Scan the QR code to open Instagram. Follow @ultima_markets to send a DM.

Open Instagram on this device.

-

Live Chat

-