This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

Learn what catastrophe bonds are. See how they work, and understand the key risks and benefits they offer insurers, governments, and investors worldwide.

Catastrophe bonds, often called cat bonds, are a type of insurance linked security used to transfer disaster risk from insurers, reinsurers or governments to capital market investors. They are usually linked to major events such as hurricanes, earthquakes, windstorms and other natural catastrophes.

For beginners, the idea is simple. Investors earn coupon payments for taking on the risk of a defined disaster. If the event does not happen, they receive their income and principal back. If it does happen and the bond is triggered, some or all of that principal can be used by the sponsor to cover losses or recovery costs.

This is what makes catastrophe bonds different from ordinary corporate bonds, where default risk is tied to a company’s finances rather than a natural event.

What Are Catastrophe Bonds

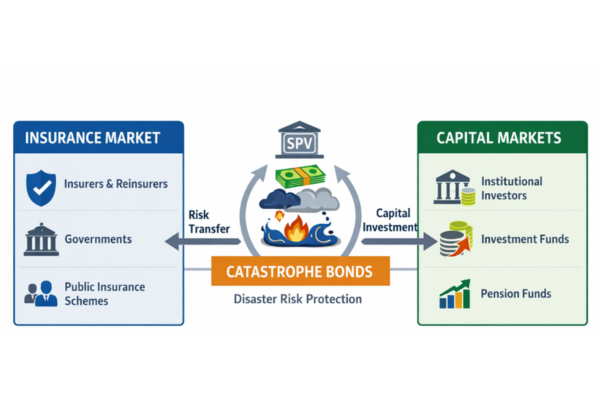

Catastrophe bonds sit between the insurance market and the capital markets. They allow a sponsor, usually an insurer, reinsurer, public insurance scheme or government, to secure protection in advance for a specific type of catastrophe risk. This can be useful when traditional reinsurance is expensive, limited or volatile.

What makes cat bonds attractive is that they are usually fully collateralised. In practice, this means investor capital is set aside upfront, so the sponsor knows funds are available if the agreed trigger is met. For sponsors, this offers extra financial resilience.

For investors, it creates access to a return stream driven mainly by disaster risk rather than broader stock market performance.

How Catastrophe Bonds Work

The basic structure

A catastrophe bond usually involves three parties. First, the sponsor wants protection against a defined risk. Second, a special purpose vehicle, or SPV, issues the bond and holds the collateral. Third, investors buy the bond and receive coupon payments for accepting the possibility of loss.

The bond is then built around a clear set of terms, including the peril, region, time period and payout conditions. For example, a cat bond might cover Florida hurricanes for three years or Caribbean cyclone risk over a multi year period. If no qualifying event occurs, investors are repaid at maturity. If a qualifying event occurs, the trigger decides whether some or all of the capital is released to the sponsor.

Common trigger types

One of the most important parts of any cat bond is the trigger. This affects how quickly the bond can pay out and how closely that payout matches the sponsor’s real losses.

Trigger type

How it works

Main strength

Main drawback

Indemnity

Based on the sponsor’s actual losses

Closely matches real claims

Can take longer to settle

Industry loss

Based on total losses across the insurance market

More transparent for investors

May not match the sponsor’s own losses exactly

Parametric

Based on measurable data such as wind speed or earthquake magnitude

Faster payout

Higher basis risk

Modelled loss

Based on catastrophe modelling after the event

Useful for complex structures

Relies heavily on model assumptions

Indemnity structures usually give the sponsor the closest protection, while parametric and index style structures may be simpler and faster but can introduce basis risk, where the payout does not fully reflect actual damage.

Why Catastrophe Bonds Matter Now

Catastrophe bonds are becoming more relevant because disaster losses remain high and are spreading beyond classic headline events. Swiss Re estimated that natural catastrophes caused USD 107 billion in insured losses across 190 events in 2025, with total economic losses of USD 220 billion.

Another key shift is the growing importance of secondary perils, such as wildfire, hail, flood and severe thunderstorms. Swiss Re said these secondary perils accounted for 92% of insured natural catastrophe losses in 2025, the highest share on record.

That matters because the cat bond market is no longer only about rare peak events like earthquakes and hurricanes. It is also adapting to more frequent and expensive weather losses.

This helps explain why sponsors keep using cat bonds. They offer another source of capacity at a time when climate related losses, inflation in repair costs and expanding urban exposure are making catastrophe risk harder to absorb through traditional insurance tools alone.

Benefits and Risks of Cat Bonds

Why sponsors use them

For insurers and reinsurers, cat bonds can diversify sources of protection and lock in cover for more than one year. That can be valuable in volatile reinsurance markets. For governments, the appeal is often faster access to emergency funding after a disaster.

A strong real world example came from Jamaica. In November 2025, the World Bank announced that Hurricane Melissa had triggered a 100% payout of USD 150 million from Jamaica’s catastrophe bond after the storm met pre agreed parametric conditions. This shows how cat bonds can provide immediate financial support when a disaster strikes.

Why investors buy them

For investors, the main attraction is diversification. Cat bond returns are usually linked to insured catastrophe events, not to corporate profits or central bank policy. That means they may behave differently from traditional equities and bonds. The trade-off is that investors are being paid to bear a genuine risk of principal loss.

The risks to understand

The biggest risk is simple. If a covered event occurs and the trigger is met, investors can lose part or all of their capital. Beyond that, there is also model risk, since catastrophe pricing depends on modelling assumptions that may not fully capture changing climate patterns, building costs or regional exposure.

There is also basis risk, especially in parametric structures. A disaster can cause serious damage, but the bond may still fail to pay if the exact trigger conditions are not met. Finally, cat bonds can be less liquid than many conventional bonds, which means exiting early may be harder during stressed market conditions.

2026 Cat Bond Market Trends

The market has grown quickly. Artemis reported that 2025 was a record year, with USD 25.6 billion of catastrophe bond issuance and an outstanding market of USD 61.3 billion at year end. It was also the first year annual issuance moved above USD 20 billion.

That momentum continued into 2026. In the first quarter alone, Artemis reported USD 6.7 billion of new risk capital across a record 35 transactions and 56 tranches, taking the outstanding market to USD 63.9 billion by the end of March 2026.

This is important to highlight. Catastrophe bonds are no longer a niche part of insurance finance. They are a growing part of the global risk transfer market, supported by strong sponsor demand and investor appetite.

Conclusion

Catastrophe bonds are designed to solve a clear problem: how to fund major disaster losses before they happen. They help insurers, reinsurers and governments transfer extreme event risk to investors, while giving those investors access to a specialised market with diversification benefits.

What makes them especially relevant today is the scale and changing nature of catastrophe risk. With insured disaster losses still above the USD 100 billion level globally and secondary perils becoming more expensive, cat bonds are likely to remain an important tool in modern risk finance.

Still, they are not simple products. Understanding triggers, basis risk, modelling assumptions and liquidity is essential before treating them as an investment opportunity or a risk management solution.

FAQs

What is a catastrophe bond?

A catastrophe bond is a security that transfers disaster risk from a sponsor to investors.

Who issues cat bonds?

They are usually sponsored by insurers, reinsurers, governments and public insurance programmes.

Are cat bonds risky?

Yes. Investors face event risk, model risk, basis risk and liquidity risk.

Share Now

Disclaimer:This content is provided for informational purposes only and does not constitute, and should not be construed as, financial, investment, or other professional advice. No statement or opinion contained herein should be considered a recommendation by Ultima Markets or the author regarding any specific investment product, strategy, or transaction. Readers are advised not to rely solely on this material when making investment decisions and should seek independent advice where appropriate.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.