This website is managed by Ultima Markets’ international entities, and it’s important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

Note: UK clients are kindly invited to visit https://www.ultima-markets.co.uk/. Ultima Markets UK expects to begin onboarding UK clients in accordance with FCA regulatory requirements in 2026.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Ultima Markets’ international entities and not by Ultima Markets UK Ltd, which is regulated by the FCA.

2.Ultima Markets Limited, or any of the Ultima Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Ultima Markets Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Ultima Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Ultima Markets wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Ultima Markets entity.

The Fed’s Last Meeting of the Year: To Pause or Further Ease?

The Fed’s Last Meeting of the Year: To Pause or Further Ease?

A Balancing Act Between Inflation and Growth

The year 2024 has been quite a roller coaster for political and economic events. The final interest rate decision meeting is scheduled for this month by the Federal Reserve. The minutes of the November meeting give insight into their next steps. A key takeaway is that many officials expressed the possibility of gradually transitioning from a restrictive to a more neutral monetary policy stance, provided economic data meets expectations—specifically, inflation steadily declining toward the 2% target and the economy maintaining near-full employment. The appearance of the term “gradually” in the meeting minutes, a significant departure from prior language, indicates the Fed is indeed slowing the pace of rate cuts.

Among these, the deletion of a confident statement about inflation moving toward 2% in the press release is particularly remarkable. It indicates that Fed officials closely watch the threat of short-term inflation stagnation and could well consider the factor while deciding on the continuity of rate cuts. Market dynamics provide further hints: the US Dollar Index has sharply risen after a two-week consolidation following the September 18 FOMC meeting, at which the Fed initiated monetary easing amidst fears of an economic slowdown. This means that the market has toned down its expectations for the pace and extent of future rate changes.

(US Dollar Index Chart)

(US Dollar Index Chart)

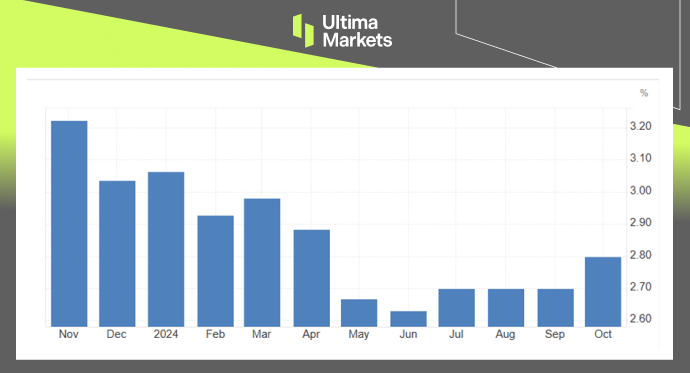

We look to a number of economic indicators for guidance on whether another rate cut is possible by year-end. The US Department of Commerce released the October PCE Index, the Fed’s preferred measure of inflation, on November 27. The annual increase of 2.3% met market expectations and was higher than September’s 2.1%. Core PCE grew 2.8% year-over-year, aligning with expectations but marking the largest annual increase since April.

Service price increases were the main driver, with core services prices, excluding housing and energy, increasing 0.4% from September, the largest monthly gain since March. Short-term inflation has been sticky, and further declines have been difficult to achieve. The annualized three-month growth rate of core PCE stands at 2.8%, still a considerable distance from the target of 2%.

(Core PCE YoY%, Bureau of Economic Analysis)

(Core PCE YoY%, Bureau of Economic Analysis)

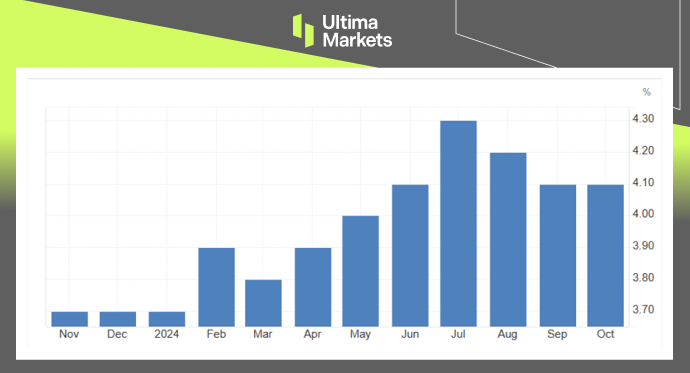

Meanwhile, the unemployment rate in October stood at 4.1% for the second consecutive month, a fact that reflects its resilience against hurricanes and corporate layoffs. In this vein, upcoming data is expected to look very good due to seasonal adjustments but show no signs of economic weakness. Other data also points to good economic health: personal spending was up 0.4% month-over-month in October, and Q3 GDP was up at an annualized rate of 2.7%, indicating strong household and business spending.

(Unemployment Rate, Bureau of Economic Analysis)

(Unemployment Rate, Bureau of Economic Analysis)

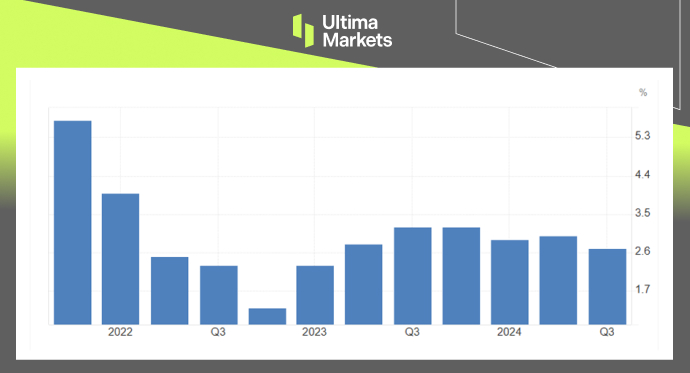

(GDP YoY%, Bureau of Economic Analysis)

(GDP YoY%, Bureau of Economic Analysis)

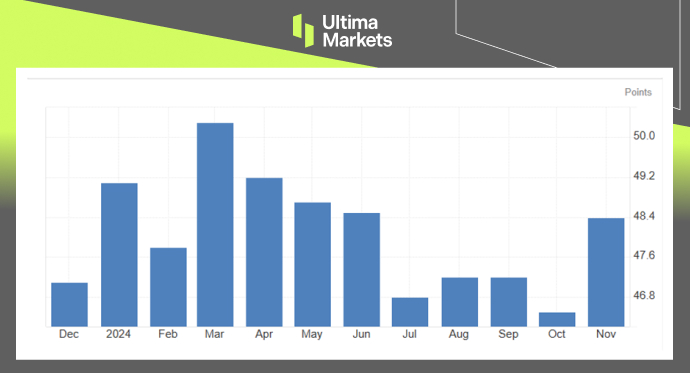

For this context, the US November ISM Manufacturing PMI came at 48.4 points, beating market expectations at 47.6 points. Thus far this year, only one result breached the 50-threshold, demarking contraction versus expansion, but closer reading again shows some encouraging trends, including a New Orders Index that leaped to 50.4 from 47.1 in the prior month—a five-month high. Even so, the sector clearly has not yet fully worked out its problems.

(ISM Manufacturing PMI)

(ISM Manufacturing PMI)

In conclusion, the Fed is likely to adopt a wait-and-see approach in December, reserving flexibility for future actions and leaving rates unchanged. If a rate cut does occur, it will likely be limited to 25 basis points, with rates expected to hold steady during the first-quarter seasonal lull, potentially allowing inflation to cool further.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.

Thank you for visiting the Ultima Markets website. Please note that this website is intended for individuals residing in jurisdictions where access is permitted by law. Ultima and its affiliated entities do not operate in your home jurisdiction.

By clicking ‘Acknowledge’, you confirm that you are entering this website solely on your own initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.