July’s job market performance fell short of expectations, according to Bureau of Labor Statistics data released August 1st. The economy added only 73,000 nonfarm payroll positions—the smallest monthly gain since October—compared to forecasts of 110,000. Historical data took an additional hit as the previous two months saw combined downward revisions of 258,000 jobs. The disappointing figures sent stocks tumbling, with the Dow losing 542.40 points, and strengthened calls for September monetary easing.

Rather than react impulsively to market turbulence, a thoughtful examination of the core issues is warranted. July saw the Fed hold rates unchanged, raising questions about potential September action. Their post-meeting statement offers insights, beginning with: “Although swings in net exports continue to affect the data, recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.”

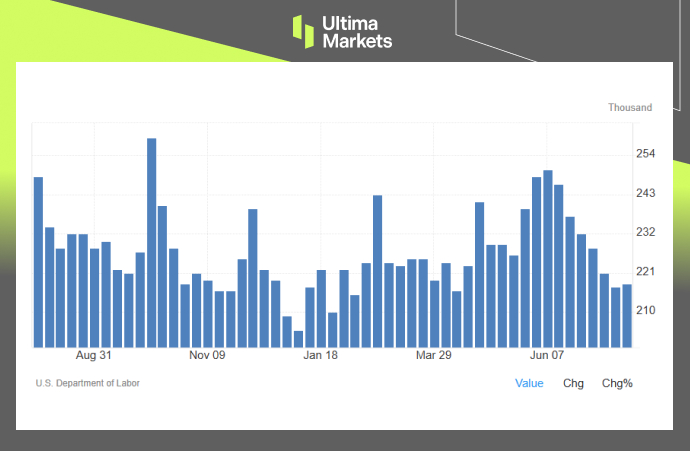

Additional employment metrics shed light on the Fed’s measured response. Weekly jobless claims for late July increased modestly by 1,000 to 218,000—remaining comfortably under the projected 224,000 and close to the three-month low recorded earlier. July’s unemployment rate edged up to 4.2% from June’s 4.1%. The Federal Reserve’s calm reaction stemmed from their June economic projections, which had already factored in labor market softening within acceptable parameters. Their median unemployment forecast was adjusted upward to 4.5% from the March estimate of 4.4%, with full-year expectations ranging from 4.3% to 4.6%.

Initial Jobless Claims (thousand),U.S. Bureau of Labor Statistics

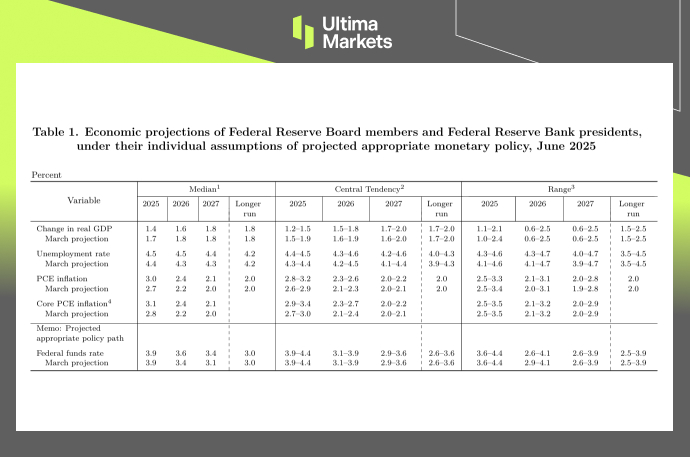

The Federal Reserve’s latest economic projections

The following paragraph declares: “The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.” This brings us to another central Fed priority – controlling inflation.

The US employs two inflation measures—Personal Consumption Expenditures (PCE) and Consumer Price Index (CPI)—to track “price shifts.” Since PCE encompasses more categories than CPI, the Federal Reserve has emphasized it since year 2000 as their primary monetary policy reference point.

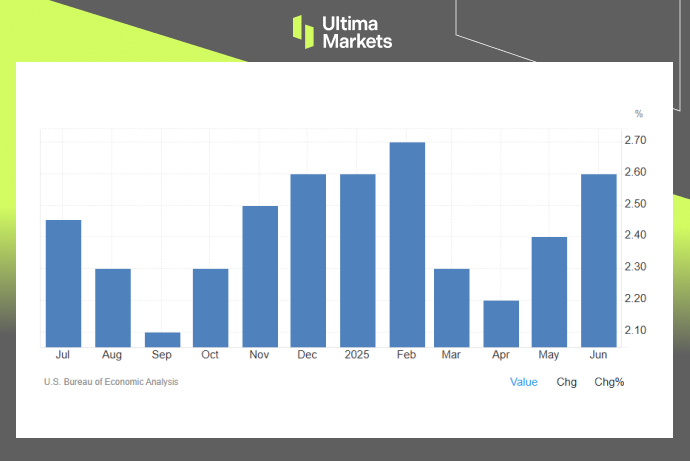

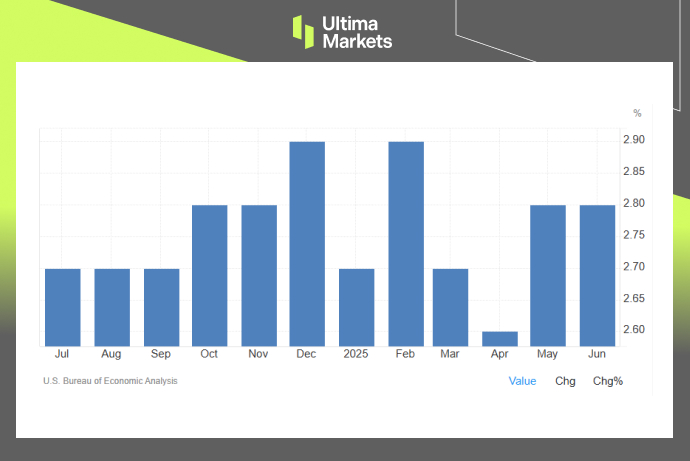

The July Personal Consumption Expenditures (PCE) report is scheduled for release on August 29th. Recent June figures revealed a 2.6% annual inflation rate, marking the highest level in four months. Additionally, the core PCE measure, which strips out volatile food and energy costs, reached 2.8%—surpassing economist forecasts of 2.7%. Meanwhile, the Federal Reserve endeavour to achieve its 2% inflation objective. Although the data suggests inflation has stabilized compared to previous peaks, it remains stubbornly above target levels and appears resistant to further decline, potentially indicating early signs of stagflation.

PCE YoY%,U.S. Bureau of Economic Analysis

Core PCE YoY%,U.S. Bureau of Economic Analysis

The United States finalized most of its import tariff rates on August 1st, However, the contentious political nature of tariff policies significantly amplifies uncertainty. The Federal Reserve has already acknowledged in its June economic projections that tariff-related effects and pricing pressures will require time to fully materialize. Officials revised their March inflation projections upward, increasing the median PCE forecast from 2.7% to 3.0% and the core PCE median from 2.8% to 3.1%, while maintaining similar full-year projection ranges. The effects of tariffs on inflation could take a good bit more time to play out, Powell said. “We’re still a ways away from seeing where things settle down,” he said. “It doesn’t feel like we’re close to the end of that process.”

The Federal Open Market Committee maintained current interest rates at its July meeting and continued to reduce its balance sheet holdings of Treasury securities and mortgage-backed securities, thereby releasing liquidity into financial markets. This strategy reflects the Fed’s approach of creating space to monitor and evaluate economic developments. Among the 12 committee members, one was absent from the meeting. For the first time in the current year, two members voted in favor of lowering rates. Despite potential nominations by President Trump for his preferred candidates, the Federal Reserve appears likely to maintain its cautious, observational stance rather than shift toward more aggressive policy changes.

The June Economic Projections Summary, under the section “Appropriate Policy Path,” kept the federal funds rate median unchanged at 3.9% from the March projection, with the annual range staying at 3.6-4.4%. Expectations for a September rate reduction remain subdued due to inflation’s stubborn persistence. Should inflationary pressures resurge, the Federal Reserve would face constrained options for response. A swift reversal of previous rate decreases could seriously undermine the central bank’s credibility. Our forecast remains cautious regarding the timing of rate reductions in the year’s latter half, anticipating perhaps only a single cut before year-end.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.